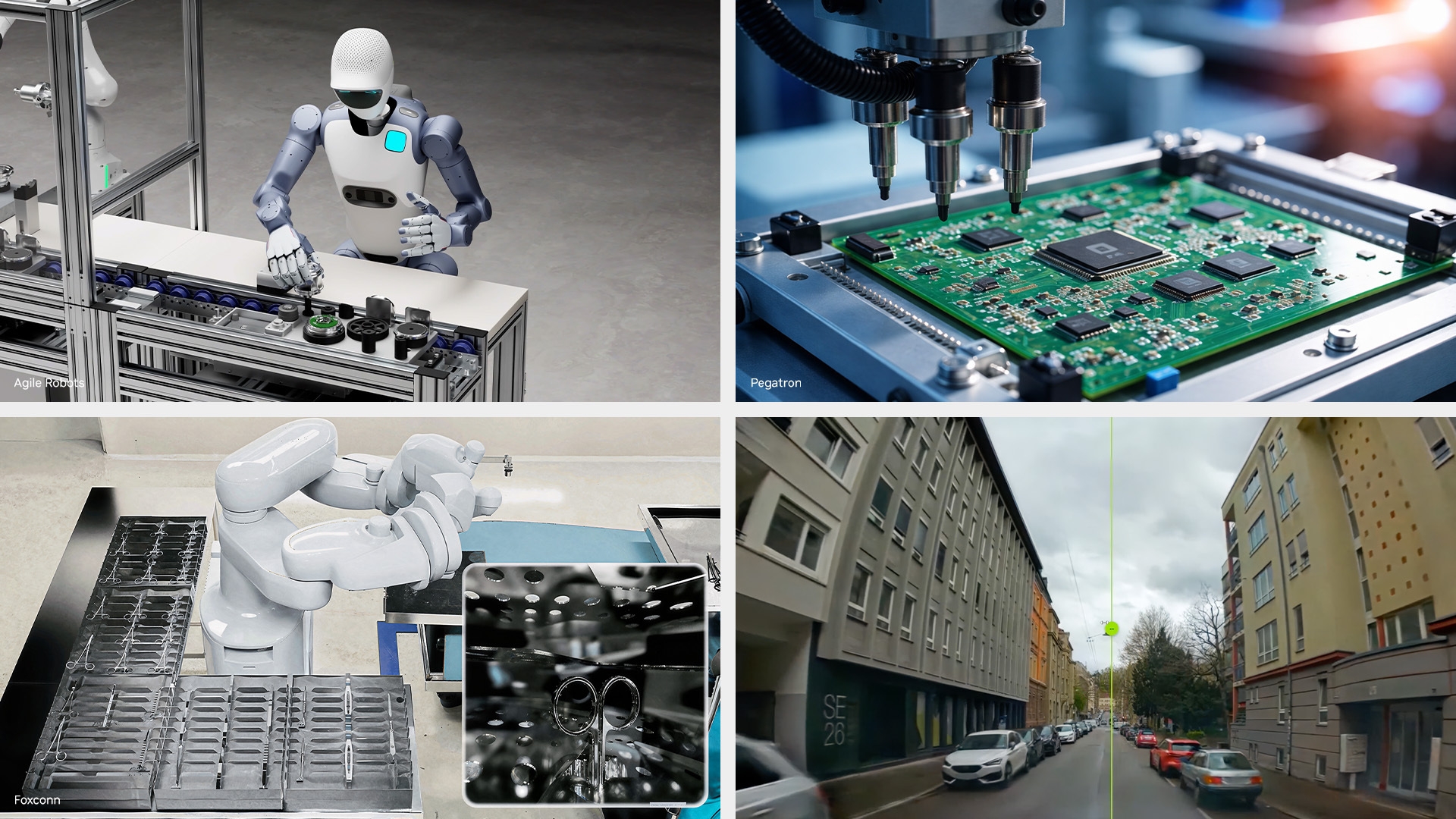

NVIDIA launched a major open-source collection of physical AI skills and tools spanning Omniverse, Cosmos, Alpamayo and Metropolis to automate robotics, AV, vision AI and industrial digital-twin workflows. The company said industry leaders including TSMC, Foxconn, Pegatron, Cadence, Siemens and others are already using the tools, with reported benefits such as Pegatron cutting training and deployment time by 67% and Delta Electronics improving defect detection by 17%. The release strengthens NVIDIA’s position in agentic AI and could accelerate adoption across manufacturing, autonomous driving and healthcare robotics.

This is less a product launch than an attempt to make NVIDIA the default operating system for physical AI workflows. The strategic value is that it shifts the moat from selling accelerators to owning the orchestration layer: once developers encode training, simulation, labeling, and deployment as reusable agent skills, switching costs rise sharply because the workflow knowledge itself becomes sticky. That favors NVDA on both gross margin durability and ecosystem lock-in, while pressuring point solutions in simulation, synthetic data, and inspection software that lack a comparable agent interface.

The second-order winner is likely the picks-and-shovels cloud layer. If physical AI development becomes more automated, usage intensity on GPU cloud and preconfigured environments should expand faster than headcount, which is bullish for MSFT, CRWV, and NBIS as distribution and capacity partners. The less obvious consequence is that industrial and semiconductor vendors may become more dependent on NVIDIA’s stack for validation loops, which could compress pricing power for independent CAD/simulation tooling over the next 12-24 months.

The near-term risk is that this is still a developer adoption story, not an immediate revenue inflection. If enterprise buyers treat the tools as experimental and keep critical workflows on-prem or on incumbent software stacks, the monetization timeline slips while sentiment remains ahead of fundamentals. A bigger tail risk is that open sourcing the skills commoditizes parts of the value chain, reducing differentiation among downstream application vendors even as it expands NVIDIA’s control point at the infrastructure layer.

Consensus likely understates how asymmetric this is for the ecosystem: the headline beneficiaries outside NVDA are not the end-users, but the platforms that can absorb the resulting compute and tooling demand fastest. The market may also be overestimating the immediacy of revenue from partners like TSM and SNPS; for them this is primarily a design-in and workflow expansion catalyst, not a same-quarter earnings driver. The best trade is to own the infra enablers and fade the smaller software names that will see more benchmark pressure than pricing power.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.74

Ticker Sentiment