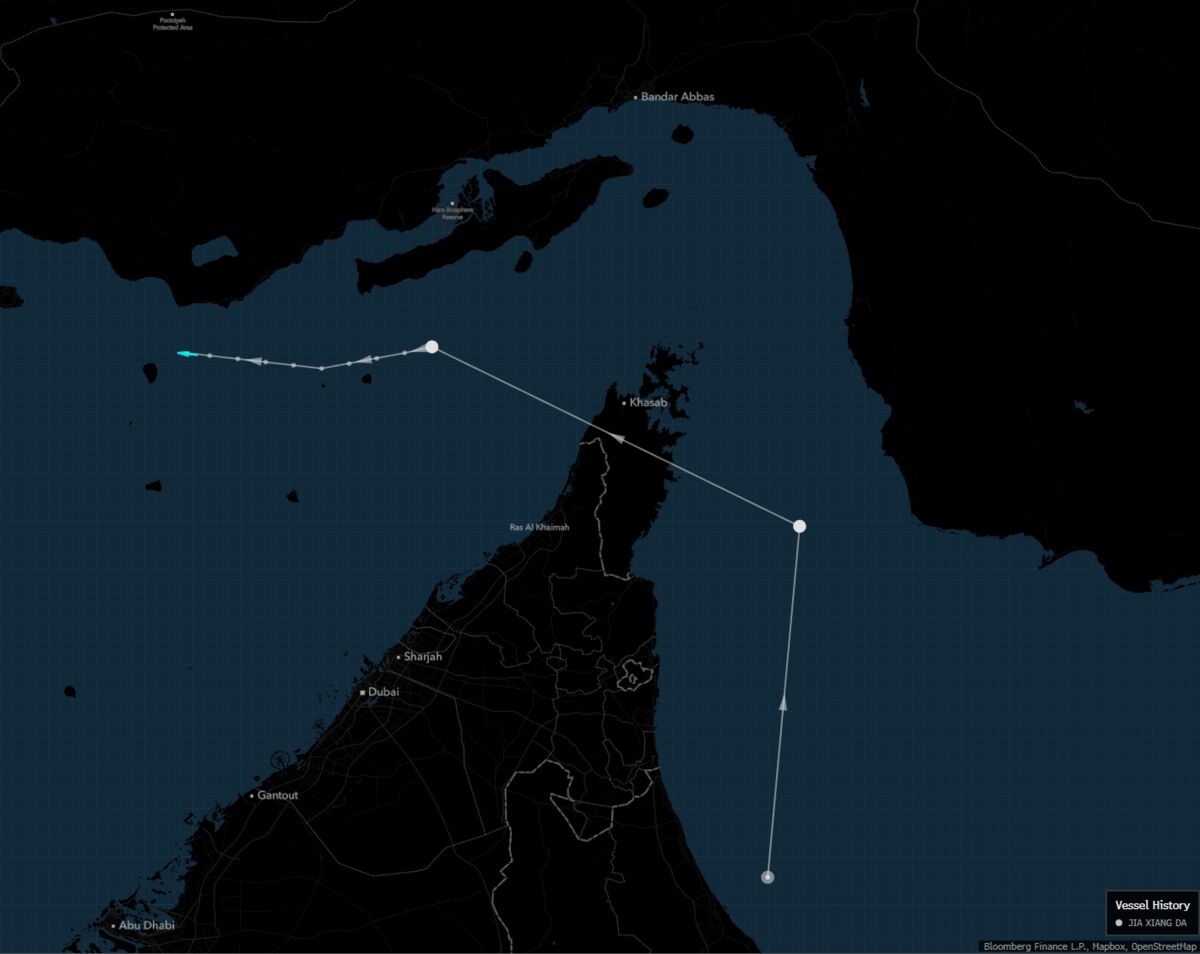

A Hong Kong-owned bulk carrier, Jia Xiang Da, transited the Strait of Hormuz into the Persian Gulf — a rare occurrence — and is due to reach Iraq’s Umm Qasr by Wednesday. Ship-tracking data show the vessel approached from the Gulf of Oman and was near the Iranian coast Tuesday en route to Kish Island; draft readings indicate the ship is empty. The transit highlights constrained navigational conditions in the chokepoint, where most passages now occur with Iran’s approval, posing localized routing and security considerations for shipping and commodity flows.

The transit should be read as tactical normalization rather than a durable de-risking of the Strait of Hormuz: commercially, it signals Iran is selectively permitting commerce while retaining leverage to throttle flows. Mechanically, that creates a regime where route availability is binary (open with permissions vs closed), which compresses the value of long-haul re-routing insurance but increases the marginal value of flexible, short-sea tonnage and operators who can take on ad-hoc regional loads.

Second-order effects center on insurance and spot freight convexity. War-risk and kidnap/piracy premiums can swing many multiples inside days when incidents cluster; historically, regional incidents produced 10–40% spikes in Handy/Panamax spot rates and a step-up in chartering premiums as owners demand compensation for risk of inspection/diversion. Because this movement involved a small, empty bulk carrier, the immediate global ton-mile shock is limited, but the signaling effect increases optionality value for owners positioned to pick up irregular cargoes (Iraq, Iran-adjacent exports).

From a catalyst and risk perspective, the setup is fragile: a single well-publicized interdiction or strike would reprice war-risk premiums and force a rapid reroute to Cape of Good Hope economics, lifting ton-miles and rates for months. Conversely, a diplomatic accommodation (quiet deconfliction or corridor agreements) would depress short-term volatility and compress premiums. Monitor insurance premium indices, Handy/Panamax FFA curves, and port call patterns into Umm Qasr/Basra over the next 2–12 weeks for confirmation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00