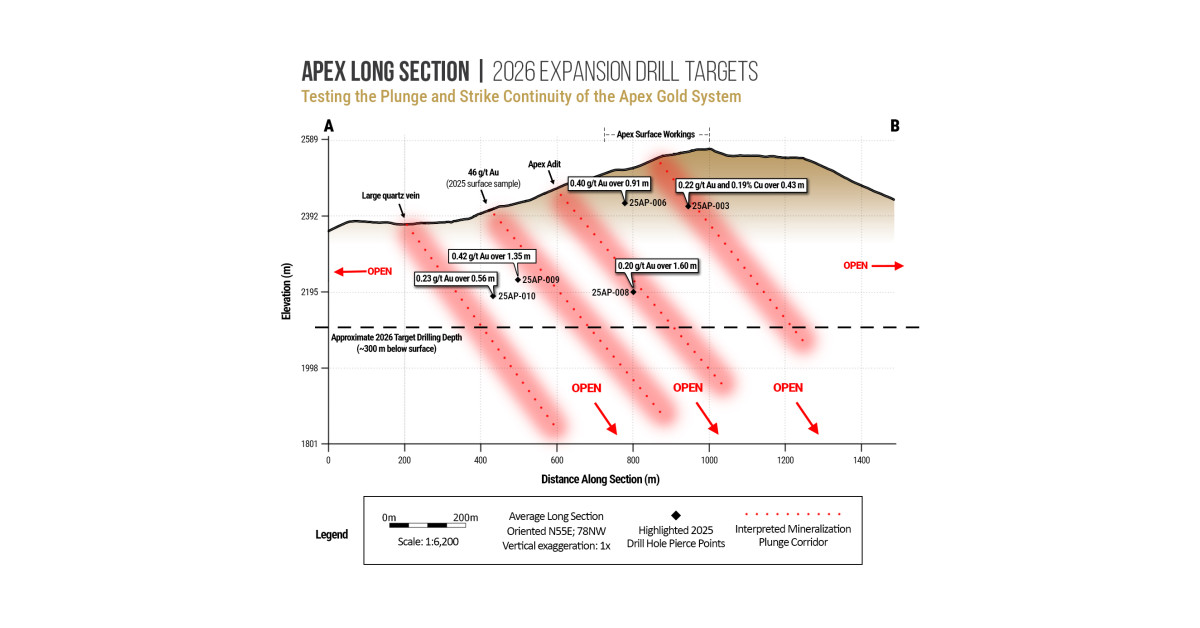

Relevant Gold launched a fully funded 2026 exploration program at its 100%-owned Bradley Peak Gold Camp in Wyoming after BLM approved an expanded five-year Plan of Operations. The program authorizes 5,000–7,000 m of core drilling to test Apex shear continuity (strike beyond ~600 m and down-plunge) and parallel structure BPEX, aiming to identify higher-grade controls and next-stage targets. While not a financial earnings catalyst, the permitting approval and planned drilling expansion are a constructive operational step that can support future resource discovery momentum.

This is a de-risking event more than a discovery event. For RGC, the immediate value is that the company has removed two of the biggest junior-explorer discount factors: access uncertainty and financing pressure. That can support a short-term rerating over days to weeks, but the equity’s true driver remains whether step-outs show continuity and whether a second shear zone actually adds scale; without that, the market will likely fade the permit/newsflow premium because the asset is still just an unproven geological option. The second-order winner is the broader U.S. gold-explorer complex, especially liquid proxies like GDXJ and SILJ, because investors tend to rotate toward permitted, drill-ready names when sector appetite improves. The flip side is that this may pull capital away from less-advanced juniors with no clear path to drilling, widening the valuation gap between ‘funded + permitted’ and ‘story-only’ names. That said, the move can be overread: more pads and a longer permit expand the number of shots on goal, but they do not improve the probability of economic ounces unless the next assays confirm higher-grade structural controls. The key catalyst path is 1-3 months: first assay batches and follow-up drill holes. If those results show weak continuity or lower-than-expected grades, the stock should mean-revert quickly because there is no near-term production or M&A floor. Over 6-18 months, the upside case is a multi-zone discovery that raises takeout optionality; the downside case is a funded but unrewarded exploration campaign that burns time and attention. Falsifier: early holes failing to extend the system or any evidence that the structural model is too diffuse to concentrate grade.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment