RTX Corporation has lowered its 2025 adjusted EPS forecast to $5.80-$5.95, citing increased cost pressures from recently heightened U.S. tariffs on steel and aluminum. This revision comes despite robust performance in its commercial aerospace aftermarket segment, which continues to see strong growth (e.g., 21% in Q1 2025) driven by rising global air traffic and continued operation of older fleets. The tariff impact also poses a risk to other aerospace firms like Boeing and Lockheed Martin, highlighting broader industry vulnerability.

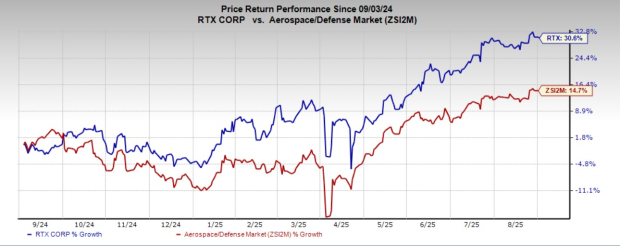

RTX Corporation presents a mixed investment profile, with robust operational performance being offset by new macroeconomic headwinds. The company's commercial aerospace aftermarket segment is a significant growth driver, recording a 21% sales increase in the first quarter of 2025 and contributing to a 9% overall organic sales rise in the last reported quarter. This strength is underpinned by favorable industry trends, including a projected 5.8% growth in global air traffic for 2025 and extended use of older aircraft fleets. However, this positive momentum is challenged by recently imposed U.S. tariffs on steel and aluminum, which have created cost pressures and forced management to lower its 2025 adjusted earnings per share forecast to a range of $5.80-$5.95. Despite this guidance revision and a southward trend in near-term consensus earnings estimates, RTX shares have appreciated 30.6% over the past year, substantially outperforming the industry's 14.7% growth. The stock currently trades at a forward P/E of 24.70X, representing a discount to the industry average of 28.04X, while the tariff issue is noted to be a sector-wide risk also affecting peers like Boeing and Lockheed Martin.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment