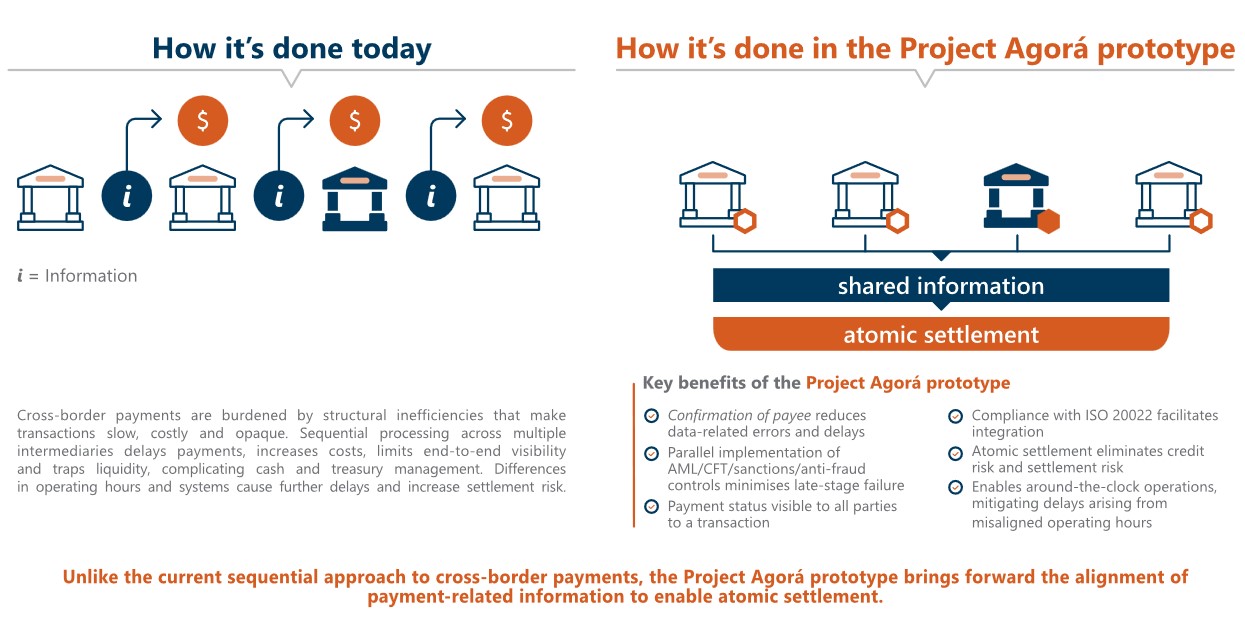

Project Agorá has delivered a prototype for atomic, multi-currency wholesale cross-border settlement using tokenised commercial bank deposits and tokenised central bank reserves. The shared platform, developed by the BIS, IIF, seven central banks and 40+ regulated institutions, could enable around-the-clock payments with smart-contract-based compliance and conditional triggers. The initiative points to lower reconciliation costs, less manual intervention and fewer payment failures, but it remains a prototype rather than a live market rollout.

This is less a near-term revenue event than a standards-setting moment: if a shared ledger for cross-border settlement becomes the default rail for banks, the economic value migrates away from messaging/intermediation and toward balance-sheet rental, compliance orchestration, and liquidity management. The biggest structural winner is likely the large global banks and custodians that can intermediate tokenized deposits and reserve access at scale; the losers are the slowest correspondent banks, niche payment processors, and any incumbent whose moat is manual ops or fragmented nostro balances. The second-order effect is tighter working-capital usage across trade finance, because atomic settlement reduces trapped liquidity and lowers the value of pre-funding buffers. The market may be underestimating how this pressures FX and payments economics over a 2-5 year horizon rather than a 1-quarter horizon. If always-on settlement becomes credible, the revenue pool shifts toward intraday liquidity, FX conversion, and embedded compliance APIs, which favors the largest bank platforms and the cloud/software vendors that provide workflow layers, while compressing take rates for legacy cross-border rails. It also creates an adoption flywheel: once a few corridors clear on a tokenized basis, corporates will push for 24/7 settlement windows, making the old batch-based model look increasingly operationally expensive. Key risk is institutional inertia: pilots often overstate interoperability and understate legal, capital, and governance friction. The biggest catalyst would be a live production corridor with meaningful volumes, while the main reversal would be a regulatory split on tokenized deposits, reserve eligibility, or finality across jurisdictions. Near term, this is mostly a long-duration optionality story; the investable edge is in picking infrastructure beneficiaries before the market fully prices the migration of payment economics away from messaging and into programmable settlement. Contrarian takeaway: the biggest upside may not be in pure-play fintechs but in banks with weak fee growth and strong deposit franchises, because tokenization can make deposits more “sticky” if they become programmable settlement instruments. That said, if the platform reduces trapped liquidity materially, the first-order beneficiary could be large corporates and trade-heavy sectors rather than payment companies, via lower cash conversion cycles and reduced fails.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35