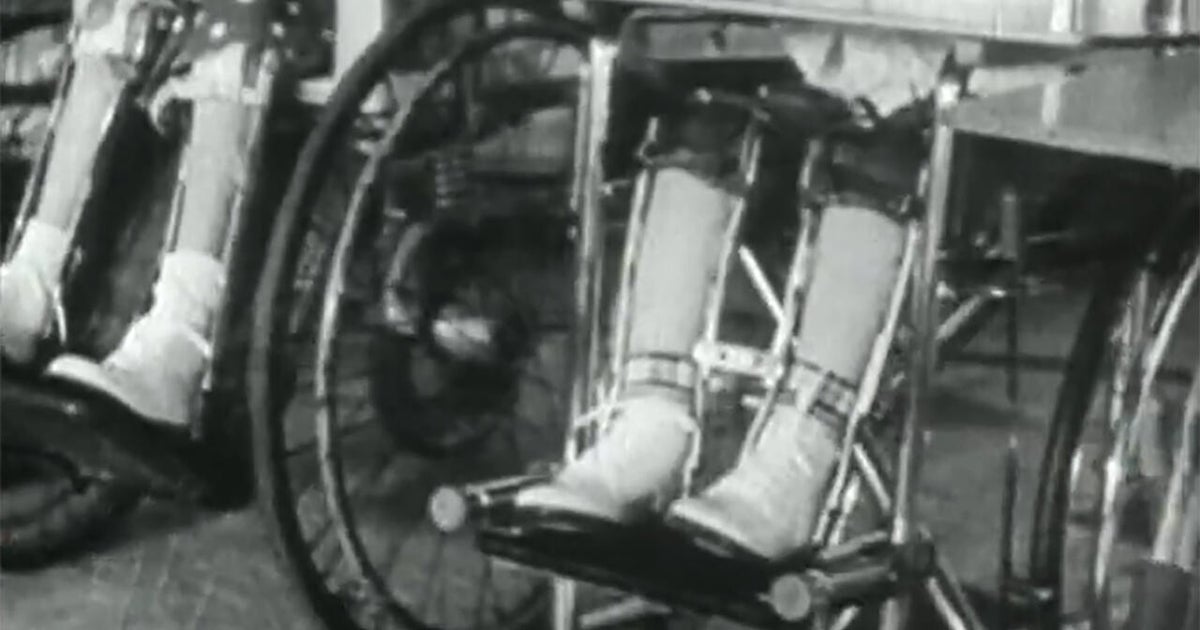

The article outlines the history and persistent risk of poliomyelitis, recounting pre-vaccine-era impacts and the development of the Salk (1954) and Sabin (1961) vaccines that drove cases down through herd immunity. It warns that rising vaccine exemptions and under-vaccinated communities create vulnerability to imported cases — citing a recent instance where an international traveler brought polio to a New York community leading to paralysis — and notes ongoing debate among public-health advisers about vaccination policy and mandates.

Market structure: A localized rise in polio risk favors vaccine manufacturers, diagnostics labs, and public‑health contractors via emergency procurements and stockpile replenishment; incumbents with scalable injectable-IPV production (large caps such as MRK, PFE, GSK) gain pricing power for supply contracts while leisure and school‑dependent services face reputational/regulatory headwinds in under‑vaccinated communities. Demand shock would be lumpy — regional state purchases of vaccines/tests could spike revenue by +5–20% for winners over quarters, but broad commercial markets remain unchanged absent a sustained outbreak. Risk assessment: Tail risks include a multi‑state outbreak (low probability, high impact) that triggers federal emergency procurement, or conversely a policy shift to weaken school vaccine mandates reducing long‑term demand; both could materialize within 3–18 months as CDC/ACIP statements and state legislation evolve. Hidden dependencies include vaccine manufacturing lead times (months), lot release/regulatory bottlenecks, and political backlash that could delay contracts; catalysts are WHO/CDC detected cases, state exemption legislation, or congressional emergency funding. Trade implications: Tactical overweight healthcare (vaccines/diagnostics) and underweight localized consumer discretionary/leisure exposure. Use capital efficient option structures to express asymmetric upside on vaccine contractors and diagnostics (3–9 month call spreads 20–40% OTM sized to 1–2% notional) while keeping 1–2% hedges short on regionally exposed leisure names (airline/cruise) for 3 months around outbreak signals. Contrarian angles: Consensus underprices the speed and cost of scaling IPV supply; a single larger outbreak could force multi‑quarter emergency buys and spike small‑cap public‑health contractors (EBS) by >50% before large caps see revenue growth. Historical parallel: measles resurgence created rapid state purchasing and legislative responses; unintended consequence — politicization may delay state purchases but increase federal stockpile contracting, benefiting federally‑connected suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment