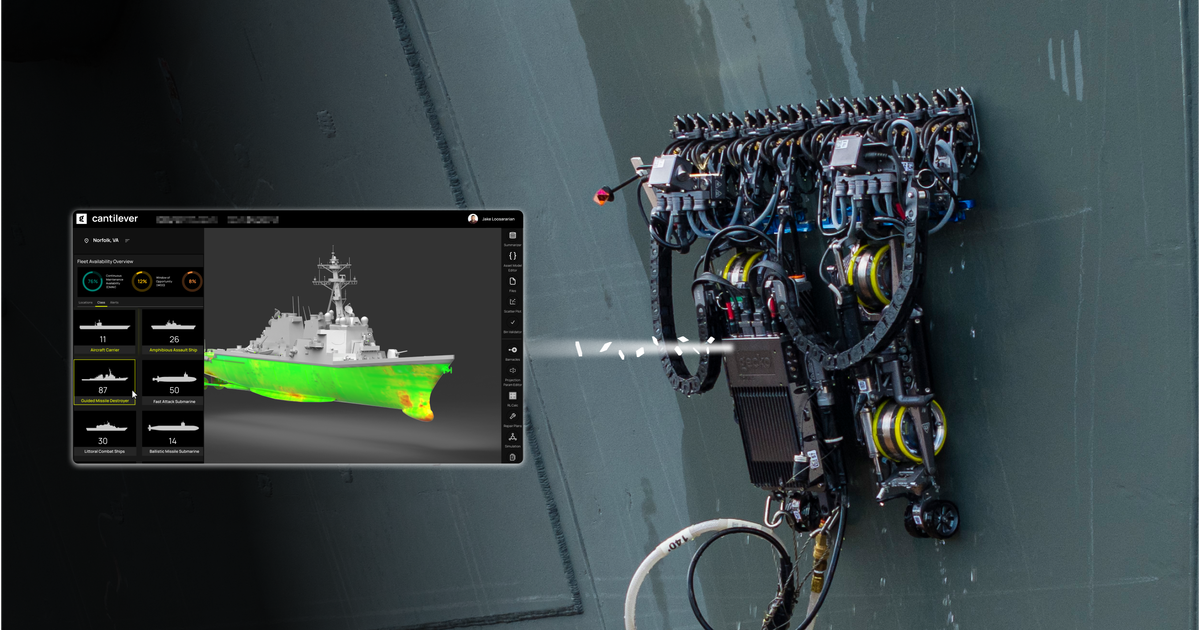

Gecko Robotics won a $71M contract to deploy its AI and robotics on 18 U.S. Navy Pacific fleet ships, with work on those ships to occur over five years. The company claims its technology can identify repairs up to 50x faster than manual methods, directly supporting the Navy's 80% readiness mandate. This deal materially validates Gecko's defense market product fit and should meaningfully increase revenue visibility and commercialization for its robots, drones and sensors.

This deployment accelerates a structural shift from periodic, labor‑intensive maintenance toward continuous, sensor‑driven predictive maintenance — a change that reallocates value from hourly dock labor and short‑term repair contracts to software, data services, and specialized hardware suppliers. Expect shipyards and primes that integrate data platforms to capture recurring revenue (analytics subscriptions, anomaly detection), while small repair outfits and inspection staffing agencies face demand erosion and margin pressure over a 2–5 year window.

Procurement and integration risk are the primary brakes: qualification cycles, cybersecurity/ITAR constraints, and Navy systems integration typically take 6–24 months to move beyond pilots, creating staging points for validation or reversal. A successful operational validation that shows measurable availability gains will be a catalyst for multi‑year follow‑on spend; conversely, any high‑visibility cyber incident or failed sea trials could pause adoption industry‑wide within quarters.

Downstream supply‑chain effects are subtle but material: demand for high‑precision sensors, edge compute, and autonomous mobility platforms will spike, tightening supply of specialty components (encoders, LIDAR/thermal arrays) and benefiting component OEMs and contract manufacturers. This also raises M&A odds — large primes will prefer to acquire or exclusive‑subcontract these capabilities rather than risk losing control of fleet readiness data.

The consensus framing — that this is a one‑off hardware sale — misses the bigger earnings lever: lifecycle data monetization and platform lock‑in. If the software/analytics layer becomes mission‑critical, expect >1.0x revenue multiple expansion for winners and consolidation activity within 12–36 months; if integration stalls, valuation reversion will be swift and concentrated among niche robotics providers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.65