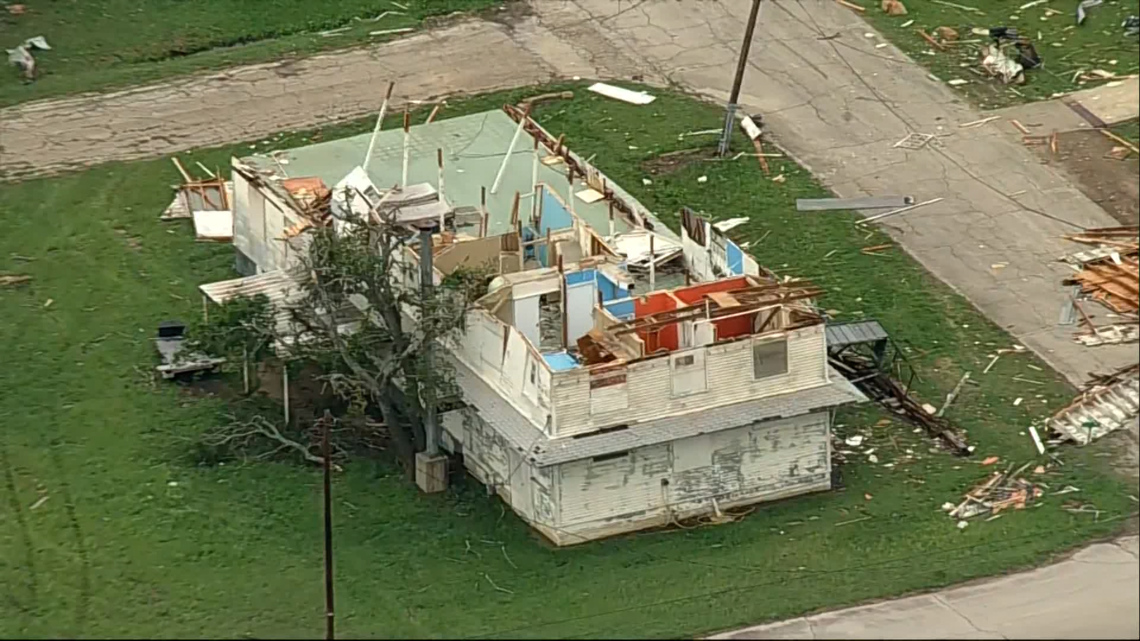

A major storm likely caused an EF-2 or EF-3 tornado in Mineral Wells, destroying homes, metal buildings, and damaging businesses across Palo Pinto County. At least two people were hospitalized, and several properties were left uninhabitable, with shelter opened at Mineral Wells High School cafeteria. The event is materially negative for local housing and infrastructure but is unlikely to have broad market impact.

The first-order economic hit is small in the context of national markets, but the second-order readthrough is meaningful for anyone exposed to weather-sensitive construction, insurance, and municipal credit. In the near term, the main beneficiaries are emergency contractors, debris removal, temporary housing providers, and regional home-improvement chains; the losers are local landlords, small-business operators, and carriers with concentrated Texas homeowners exposure. The key nuance is that losses will likely be concentrated enough to create localized margin pressure for insurers and reinsurers without immediately changing broader underwriting assumptions, which tends to show up later in reserve reviews rather than headline catastrophe estimates.

For housing and real estate, the event is a demand reset more than a demand destroyer. Rebuild activity can create a multi-quarter bump in roofing, HVAC, lumber, and portable shelter demand, but only after the claims process unlocks capital; that lag is often 60-120 days and can overlap with higher labor and materials inflation. If this damage is validated as EF-2/EF-3, expect a short-term spike in permit activity and contractor utilization, followed by a longer tail of affordability stress if displaced households remain in temporary housing and local rental vacancy tightens.

The contrarian angle is that markets often underprice the municipal and credit spillover versus the visible property damage. Smaller Texas municipalities and school-adjacent infrastructure can face unplanned cash needs, while local banks with outsized exposure to construction and consumer loans may see subtle credit deterioration before headline defaults appear. If federal/state aid is delayed or claims processing is slow, the dislocation can extend from days into months, which is where the opportunity is for relative-value trades rather than outright disaster hedges.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.70