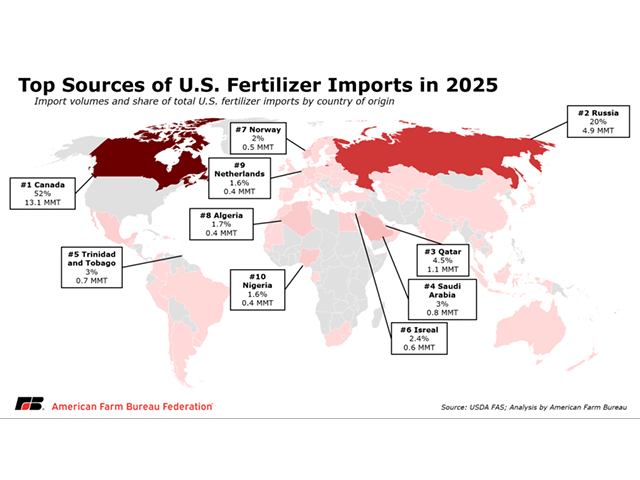

Urea prices have jumped ~25% from $465/ton on Feb. 27 to $580/ton, and Brent crude briefly hit $110/bbl (vs. ~$72 before Feb. 28 strikes), intensifying input-cost pressure ahead of U.S. spring planting. AFBF warns higher urea and diesel costs could add roughly $100/acre for some growers and cited cases of ~$200/ton uplifts that increased bills by ~ $20,000 for individual farmers; the U.S. imports ~5 million MT of urea with Russia and Qatar as top exporters. The Farm Bureau urged President Trump to protect Strait of Hormuz shipments, suspend countervailing duties on fertilizer, waive the Jones Act, and use other trade and shipping measures to avert broader food-supply and inflation shocks.

Immediate winners are firms that own production and pricing power in fixed-nitrogen and phosphate chains; they can convert a logistics-driven spot premium into margin within weeks because manufacturing is globally concentrated and contracts are often short-dated. Distributed intermediaries and dealer networks are second-order losers: they face working-capital squeezes (pre-paid inventory being re-priced by sellers), reputational risk with farmer clients, and higher receivables funding needs that will surface in near-term cashflow statements.

Logistics and financing are the choke points that determine whether a price spike is transitory or persistent. A naval/insurance solution or temporary tariff relief would collapse the risk premium inside 2–8 weeks by restoring routings and lowering freight and credit costs; conversely, sustained insurance-cost increases, port bottlenecks, or insurance exclusions would force buyers to compete for inland inventories through planting season, extending elevated margins into the 2–6 month window.

Macro cascades matter: acreage shifts away from nitrogen-intensive crops will reduce fertilizer demand next planting cycle and create a 6–18 month mean-reversion tail for producers’ pricing power. That makes option structures and relative-value trades preferable to naked directional exposure — you want to capture an outsized upside if premiums persist while limiting downside if policy or de-escalation normalizes markets quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.60