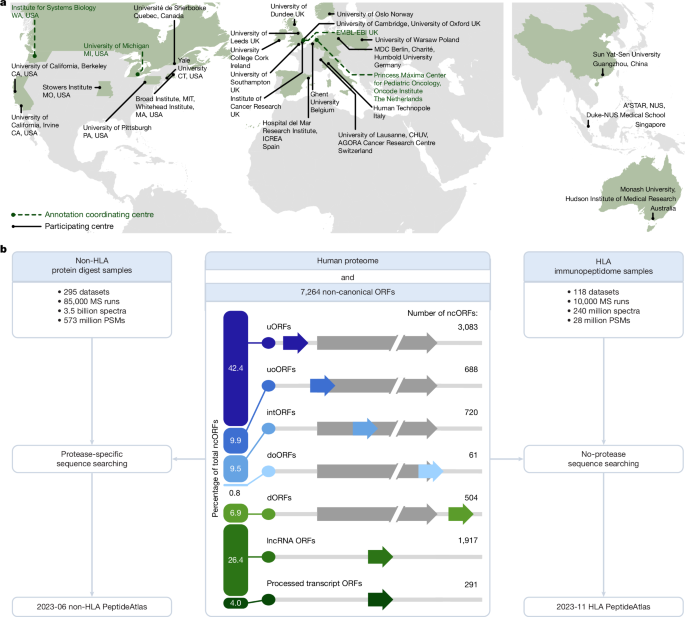

The article reports a multi-consortium scientific advance that expands the human proteome framework by identifying protein-level evidence for 25% of 7,264 ncORFs in large-scale proteomics and immunopeptidomics datasets. It introduces a new annotation class, “peptideins,” and flags several ncORFs as candidates for future protein-coding gene status, including GMCL1 and OLMALINC-derived products with functional evidence. The work is important for biotech and genomics research, but it is academic in nature and is unlikely to move markets directly.

The real investment signal is not “more biology,” it is a re-pricing of the bottleneck in therapeutic discovery: once translation evidence becomes machine-curated at scale, the scarce asset shifts from finding obscure peptides to proving function, tissue selectivity, and manufacturability. That favors platforms that can move quickly from discovery to validation—proteomics tooling, targeted MS workflows, single-cell perturbation analytics, and immunopeptidomics-enabled discovery—while commoditizing generic database-search software and broad transcript-only annotation pipelines.

Second-order, the paper strengthens the case for a larger near-term market in cryptic antigen and microprotein workflows than in traditional de novo protein annotation. The highest-probability commercial path is cancer immunotherapy and biomarker enrichment, because immune presentation data creates a lower-friction validation layer than classic enzymology or structural biology. That should pull budget toward firms with sample prep, targeted MS, HLA/immunopeptidomics, and AI-driven peptide scoring; the upside is in tools and consumables, not yet in obvious single-asset therapeutics.

The contrarian miss is that this is likely to increase, not decrease, the burden of evidence. Most newly surfaced candidates will fail to graduate from “peptidein” to druggable protein, so the near-term revenue impact is mostly on discovery spending rather than approved-product demand. The tail risk is that the field remains academically exciting but commercially slow if regulators and curators do not accept HLA evidence as sufficient, which would cap the annotation-driven re-rating and keep monetization confined to research-use-only channels for years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35