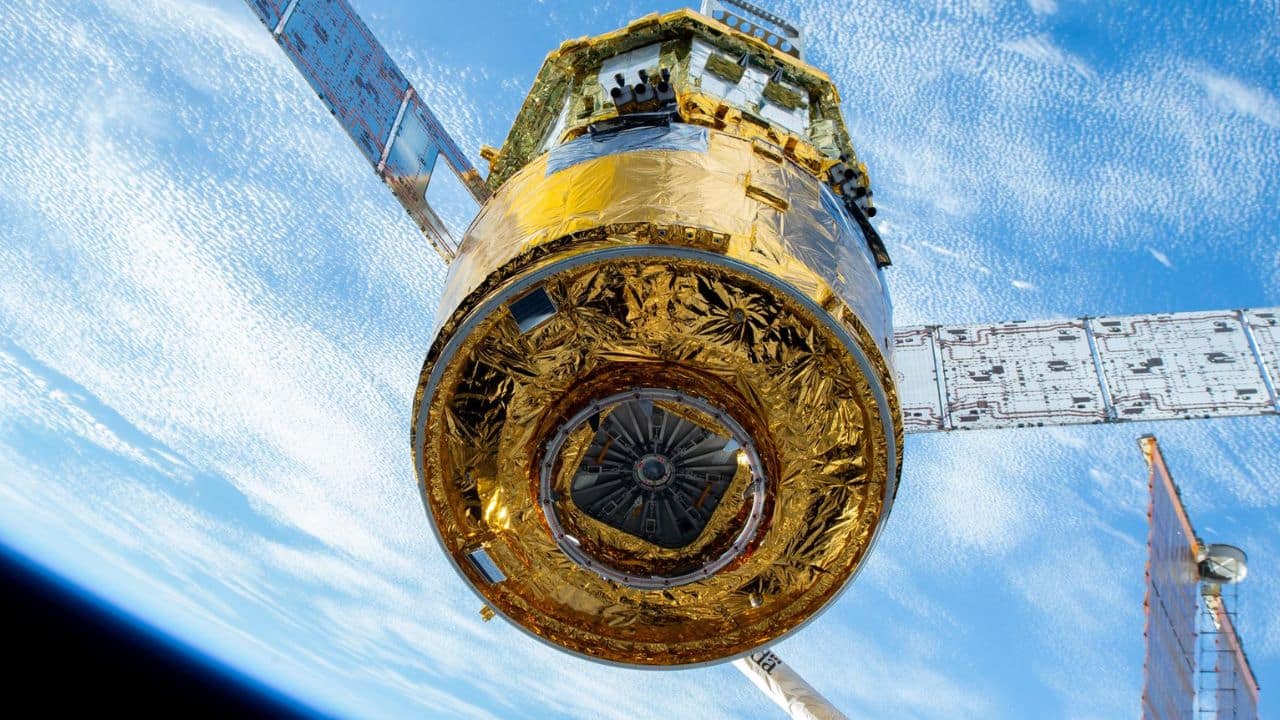

HTV‑X1, an uncrewed Japanese cargo spacecraft that launched in October 2025 and delivered roughly 12,000 pounds of supplies and hardware to the ISS, is scheduled to depart the station on 6 March 2026 with live coverage beginning at 11:45 a.m. EST and release at 12:00 p.m. EST. NASA flight controllers will use Canadarm2 to detach the vehicle from the Harmony module while an astronaut monitors systems; HTV‑X1 will then remain in orbit for over three months hosting JAXA experiments before a commanded destructive reentry to dispose of several thousand pounds of trash. The event highlights continued NASA–JAXA logistics cooperation and Japan’s cargo capabilities but carries minimal near‑term market implications beyond potential operational impacts for contractors and suppliers.

Market structure: HTV‑X1’s smooth mission reinforces incumbents in government cargo/logistics — suppliers and prime contractors tied to JAXA and NASA (e.g., Mitsubishi Heavy Industries 7011.T, Northrop Grumman NOC, Lockheed LMT, Maxar MAXR) are modest beneficiaries as perceived program risk falls. Pricing power is limited (government buyers) but contract flow and aftermarket services (on‑orbit experiment platforms, deorbit disposal) increase recurring revenue visibility by low double digits over 12–36 months for proven suppliers. Supply/demand: incremental demand is small vs. global launch capacity, but steady ISS/logistics spend supports defense/aerospace MRO and parts suppliers; commodity impact is negligible (<1% demand delta for aluminum/titanium). Cross‑asset: expect tiny tightening in credit spreads for high‑grade aerospace suppliers (bps range), negligible FX impact; small uplift to IG aerospace bond prices and reduced idiosyncratic volatility for large primes over 3–12 months.

Risk assessment: Tail risks include an operational failure or reentry debris claim leading to reputational/legal costs (> $100M) and higher insurance premiums across launch/supply chains. Immediate (days): event risk around the undocking broadcast; short (weeks–months): JAXA/NASA contract awards and budget cycles (monitor US FY2027, JAXA procurement through Q2 2026); long (quarters–years): ISS lifetime decisions and commercialization (could shift >10–20% of cargo spend to commercial players). Hidden dependencies: contractor subcontractor concentration, export control/geopolitical policy changes, and liability regimes for deorbiting waste.

Trade implications: Favor large-cap primes with strong balance sheets and recurring government revenue; use 6–12 month horizons to capture contract awards and rerating. Consider relative value: long NOC or LMT vs short speculative small-cap launchers (RKLB) to exploit funding/price pressure; options can be used to lever upside (buy calls or call spreads) while capping downside. Rotate modestly into Aerospace & Defense (XAR/ITA) and away from speculative pure‑play launchers until clearer procurement signals (3–6 months).

Contrarian angles: Market underprices Japan’s exportable logistics IP — sustained HTV‑X cadence could open commercial cargo/export contracts with private stations, implying >20% incremental TAM over 3–5 years for Japanese suppliers. Reaction is currently underdone: equities of primes may reprice positively if JAXA moves to commercialize HTV variants. Historical parallel: SpaceX Dragon’s early successes cascaded into multi‑billion awards for partners; a similar, smaller scale uplift is plausible for MHI/NOC. Unintended consequence: faster commercialization could compress margins for pure integrators but expand aftermarket services for well‑capitalized primes.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.10