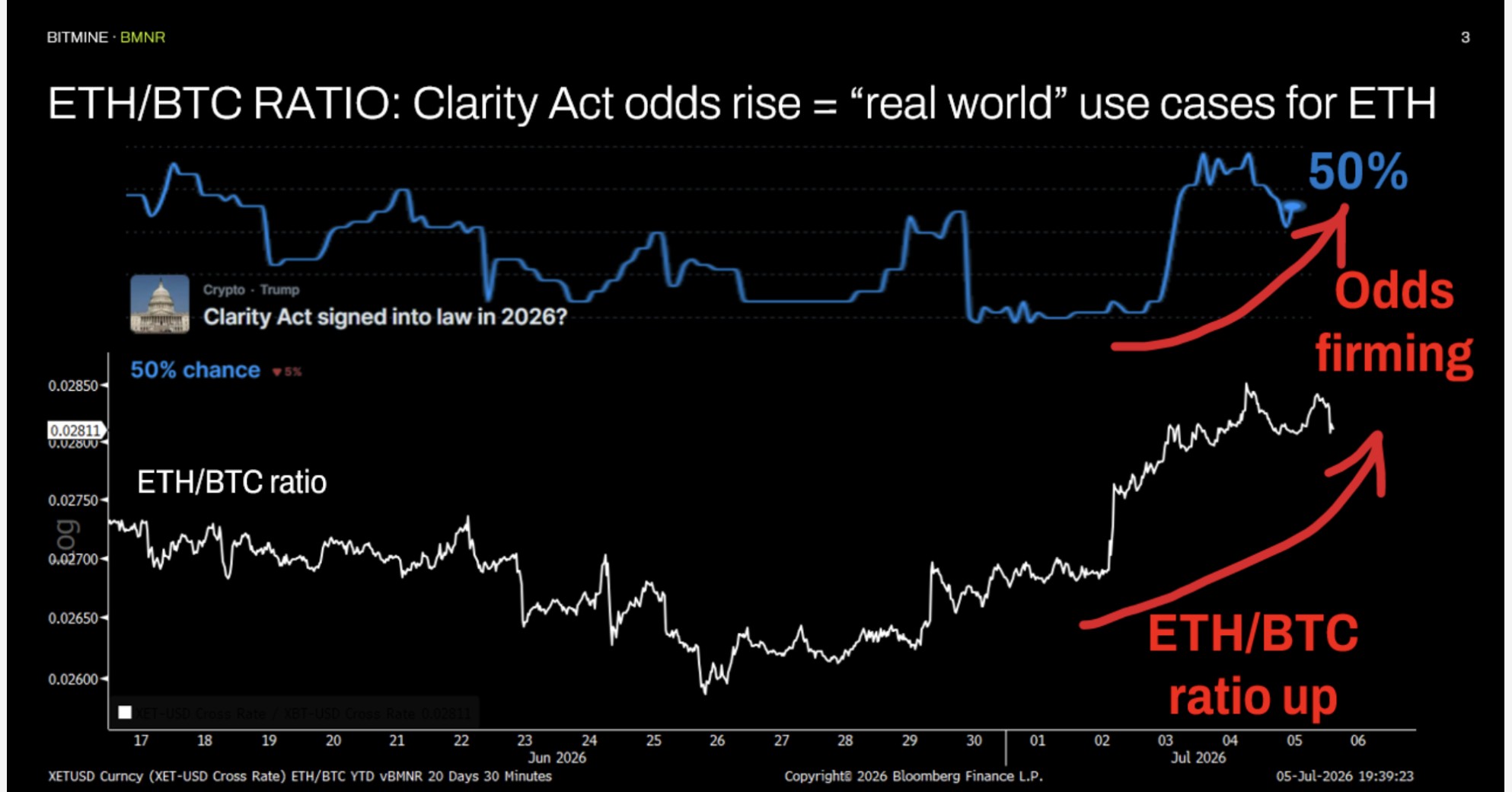

Bitmine reported an ETH-treasury of 5,742,237 ETH (~$10.3B at $1,800/ETH), alongside 206 BTC and total cashable liquid assets of $527M, positioning the company as the largest ETH treasury globally. The company raised net proceeds of ~$273.8M (3.5M Series A preferred shares at $80, 9.50% coupon) and disclosed staking scale of 4,879,157 ETH (~$8.8B), with annualized staking earnings now estimated at ~$235M (up to ~$277M if fully staked via MAVAN). Management links improving sentiment (Clarity Act pass probability ~50%) and upcoming regulation (GENIUS Act/SEC Project Crypto) to potential upside for Ethereum L2 usage, while Russell 1000 entry is expected to add hundreds to thousands of institutional holders.

BMNR is increasingly a leveraged Ethereum wrapper with a staking overlay, not a traditional miner. The key market mechanism is balance-sheet optionality: if ETH stays bid, the company can keep issuing against a rising asset base and force investors to choose between paying up for scarcity or being diluted by supply. That makes the stock’s upside convex, but it also means the implied equity value can outrun the underlying cash-yield economics very quickly. The beneficiaries of a real Ethereum-regulatory repricing are the infrastructure names, not the headline token holders. COIN gains from deeper liquidity, custody, and staking monetization; V and SHOP only matter if onchain settlement migrates from demo traffic to meaningful checkout volume, which is a 6-18 month adoption path and likely immaterial to near-term earnings. MSTR is a relative loser in any rotation where public-market capital starts preferring ETH smart-contract exposure over BTC scarcity exposure. The contrarian risk is that this is becoming a crowded narrative trade: index inclusion and legislative optimism can create a technical bid, but they do not remove dilution, funding, or execution risk. If ETH/BTC rolls over, BMNR should de-rate faster than ETH because investors are buying a premium vehicle with governance and capital-raising risk layered on top. Falsifiers to watch are a failed ETH/BTC breakout, a collapse in the BMNR premium-to-NAV, or any delay that pushes Clarity Act odds back materially below current levels.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment