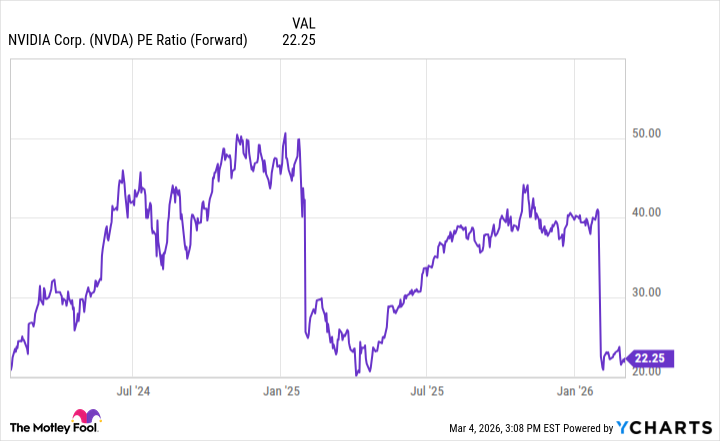

Analysts project Nvidia to grow revenue ~70% to over $360B in fiscal 2027 with profit margins above 50%; the stock currently trades ~22x forward earnings vs a historical 40–50x range. A re‑rating to ~45x forward EPS would roughly double the share price; the author expects continued hyperscaler AI infrastructure spending (estimates through at least 2030) and a sentiment-driven rerating through 2026 despite near‑term market caution.

The most important pathway to a material re-rate is flow and scarcity rather than pure unit economics — a visible acceleration in order cadence from non-hyperscaler markets (telco, utilities, defense) or a clear expansion of supply (additional capacity windows at foundries) will flip sentiment quickly because it reduces the binary "supply-constrained winner takes all" narrative. Conversely, any signs that cloud customers are internalizing inference/training workloads or that a meaningful portion of demand is shifting to more commoditized accelerators will compress optionality and cap the multiple investors are willing to pay.

Second-order beneficiaries include capital equipment and packaging suppliers whose lead times shorten ASP elasticity (they get pricing power when fabs are capacity-constrained) and DRAM/HBM vendors where tighter supply cycles translate into higher module pricing and mix improvement; losers include aftermarket OEMs and reseller channels that rely on inventory turns and price parity with hyperscalers. Expect margin volatility at the component level to precede valuation moves at the OEM level — improved component margins generally translate into outsized FCF beats within 2–4 quarters as production scales.

Key risks are idiosyncratic and policy-driven: export control escalations, a benign-but-swift slump in cloud capex, or a credible in-house accelerator that meaningfully erodes pricing power are event risks that can compress the multiple faster than fundamentals move; these tend to show up first as rising dealer inventory and elongating lead times in supplier reporting. Near-term catalysts to watch are (a) channel inventory disclosures from large cloud buyers and distributors, (b) margin and ASP commentary from packaging/foundry partners, and (c) pronounced shifts in option market flow (sustained buying of long-dated calls that signals institutional conviction). Time horizon: manage positions across 3–18 months depending on whether you’re trading re-rate momentum or structural adoption.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.65

Ticker Sentiment