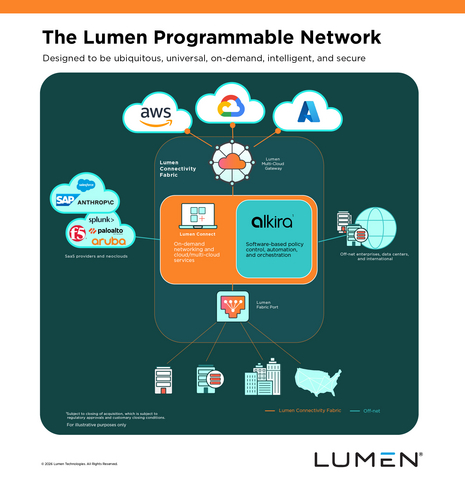

Lumen agreed to acquire Alkira for $475 million in an all-cash deal, adding a cloud-native control plane to its fiber network and expanding its enterprise networking platform. Management says the transaction should be neutral to margin in the near term, accretive as the platform scales, and could lift Lumen’s total addressable market to about $70 billion. The deal is expected to close in Q3 2026, pending regulatory approvals.

This is less an acquisition story than a repositioning of LUMN from bandwidth seller to workflow platform, and the market should treat that as a multiple event rather than a near-term earnings event. The key second-order effect is on mix: if LUMN can wrap higher-level orchestration around its fiber, it can monetize the same physical asset multiple times through control-plane fees, which is the difference between commodity transport and software-like recurring revenue. That said, the integration burden is real; the value hinges on whether sales cycles shorten enough to offset the friction of combining enterprise telecom and cloud-native procurement motions.

The bigger winner may be LUMN’s ecosystem rather than LUMN alone. Cloud interconnect, security, and managed-service partners that plug into a single orchestration layer should see higher attach rates, while pure-play WAN and SD-WAN vendors face pricing pressure as routing/policy management gets abstracted into one pane. In parallel, international expansion via carrier-agnostic overlays is capital-efficient, but it also raises the odds of indirect competition with hyperscaler networking constructs and regional carriers that currently capture off-net margin.

The main bear case is timing: the strategic payoff is probably 12-24 months out, while integration risk and customer migration happen immediately. If the market was already pricing LUMN as an operational turnaround, this can be additive; if not, it may be read as another execution-heavy pivot that delays deleveraging. The contrarian read is that the deal is less about TAM expansion and more about reducing the probability that LUMN remains stuck as a low-growth infrastructure utility; that could matter more to equity duration than to current-quarter fundamentals.

Catalysts are clear: investor call guidance on integration milestones, cross-sell timing, and any indication of margin neutrality beyond the near term. The biggest reversal trigger would be a slower-than-expected regulatory process or evidence that enterprise customers view the combined stack as too early-stage to standardize on, which would push the payoff into 2027 and compress any re-rating. Near term, the stock likely trades on narrative credibility, not modeled synergies.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.72

Ticker Sentiment