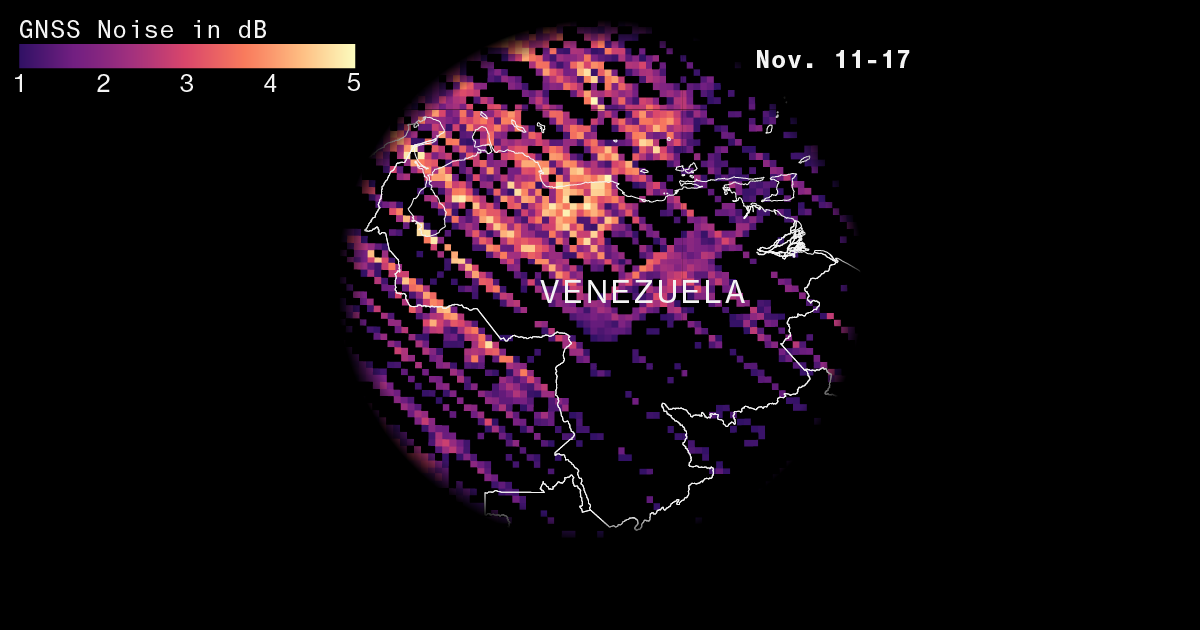

Widespread GNSS jamming over Venezuela has degraded satellite navigation and ADS-B reporting, prompting the FAA’s Nov. 20 warning and the suspension of international carriers including Avianca, Iberia and Gol; Spire data show over 10% of air traffic in the sector was operating with compromised navigation prior to the advisory. NASA CYGNSS imagery and contemporaneous interference spikes coincide with a US naval buildup—including the mid-November arrival of the USS Gerald R. Ford—and strikes on suspected drug-running vessels, heightening military-electronic activity that also risks impacts to LEO satellite constellations. The disruption exposes reliance on weak L1 GPS avionics across the global fleet (with limited L5 upgrades), elevating operational, insurance and regional geopolitical risk for airlines, satellite operators and defense contractors.

Market structure: Immediate winners are defense/electronic-warfare and avionics retrofit suppliers (L3Harris LHX, Northrop NOC, RTX RTX, Honeywell HON, Garmin GRMN) plus niche satellite/ADS-B data providers such as Spire (SPIR) as airlines seek independent surveillance. Losers are international carriers with Venezuela/Caribbean exposure (GOL, IAG) and insurers/air-freight integrators; expect pricing power for fast-build EW contractors and retrofit vendors as procurement windows compress over 3–18 months. Cross-asset: risk-off will likely push USD/Treasury flows (yields down ~10–25bp in acute episodes), EM FX (BRL, COP) weaker by 1–4%, and oil +1–4% on shipping risk; airline equity vols will spike near-term. Risk assessment: Tail risks include kinetic escalation closing Caribbean air/sea lanes (10–15% probability over 3 months), widescale GNSS cyberattack affecting financial/timing infrastructure (low-probability, high-impact), and sanctions that could block suppliers (policy risk). Immediate (days): flight reroutes and earnings hits for carriers; short-term (weeks–months): accelerated RFPs for EW/receiver upgrades; long-term (1–3 years): fleet-level L1→L5 retrofits and ground-system investments. Hidden dependencies include timing/settlement systems and logistics networks that rely on GNSS, creating second-order operational risk across banking and power grids. Trade implications: Direct plays — establish idiosyncratic long exposure to LHX/RTX/NOC (2–3% position each) and a tactical 1–2% long in SPIR to capture data/ADS-B demand; reduce/short LATAM-exposed carriers (1–2% short GOL, and consider trimming IAG by 50%). Use options: buy 3–6M call spreads on LHX/NOC (15–25% OTM) to cap premium and buy 3M puts on GOL (20% OTM) as asymmetric hedge. Rotate portfolio overweight to defense/avionics and underweight travel/leisure EM for 3–12 months; enter within 1–14 days and trim on a 25–35% realized gain or rapid de-escalation within 90 days. Contrarian angles: Consensus underestimates multi-year capex: retrofit demand could create a $1–5bn addressable market over 1–3 years for avionics/EW suppliers, which is likely underpriced versus near-term newsy weakness in defense names. Conversely, markets may over-penalize SPIR/LEO operators despite being potential beneficiaries of demand for independent PNT/surveillance — a 10–20% mispricing is plausible. Historical parallels (Ukraine GNSS jamming) show procurement cycles and regulation follow quickly; unintended consequence: insurers/regulators mandating upgrades could accelerate revenues but also concentrate counterparty risk among a few suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

Ticker Sentiment