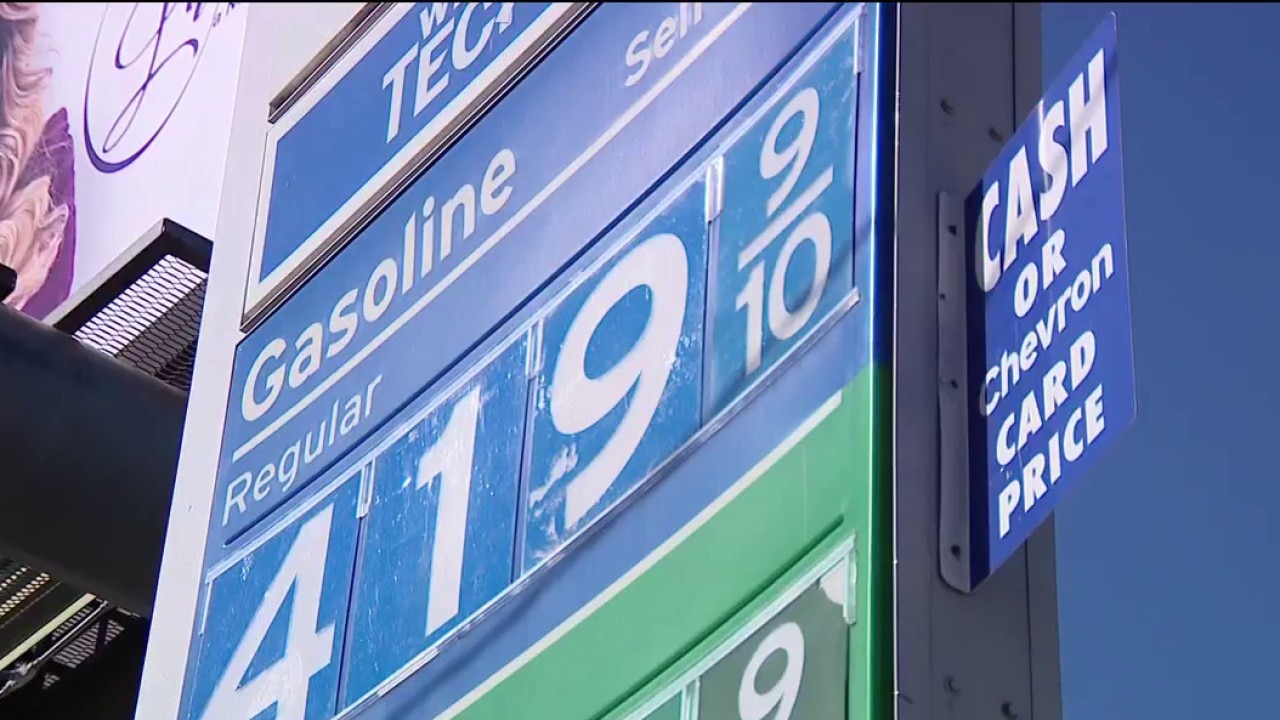

Average gas prices in Hillsborough, Pinellas, Pasco and Sarasota counties are sitting just under $4/gal, and Citrus County has crossed $4/gal, per AAA. Rising fuel costs are forcing small businesses to raise delivery fees (example: Mona's Floral Creations moved delivery from $10 to $12 to $15 and may temporarily increase to $18) and to change operations (grouping route deliveries) to curb fuel expense. The price pain is creating visible consumer friction around the $4 anchor and could squeeze local small‑business margins ahead of seasonal demand such as Mother's Day.

The mental-anchor effect of a round-number fuel price (the $4 psychological threshold) is a short-run demand amplifier: consumers notice gas at the pump and immediately reclassify discretionary micro-spends (same-day deliveries, impulse retail, low-margin eating out). Expect a measurable pullback in frequency of low-ticket, delivery-dependent purchases in the coming 2–8 weeks as consumers test new reference points; conversion elasticity for these micro-transactions is likely several multiples higher than aggregate gasoline consumption elasticity, so revenue impacts for “impulse + delivery” SMEs will be nonlinear versus the headline fuel move.

For small businesses that operate thin margins and price-by-delivery (florists, independent restaurants, local retailers), a 20% step-up in a delivery fee (e.g., $15 to $18) functions like a discrete tax on order incidence. Behavioral price sensitivity and operational responses (batching routes, longer hold times) compress same-day fulfilment and increase inventory dwell; that creates a seasonal risk into Mother’s Day where demand is concentrated and input-cost uncertainty raises working-capital needs and potential spoilage losses for perishables.

Scale winners are clear: national platforms and carriers with dynamic routing, hedged fuel exposure, or the ability to reprice delivery (Amazon, Uber/Grubhub, large grocers) can internalize or pass through costs and grab share from independents. Second-order beneficiaries include route-optimization and dispatch SaaS vendors whose short-term sales spike as small operators buy consolidation tools; refiners/retail fuel spreads and fuel futures gain modestly, but political/SRP interventions remain the biggest exogenous downside risk.

Key catalysts and timeframes: near-term volatility (days–weeks) driven by refinery maintenance, regional supply tightness, and weather; medium-term (1–3 months) effects hinge on crude price direction and national inventory moves; reversal is plausible if crude falls, refineries add gasoline yield, or policy/logistics interventions blunt local pump spikes. Tail risk is sustained regional pump inflation that accelerates substitution away from same-day services and permanently compresses SME market share — a multi-month structural issue rather than a single-event noise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment