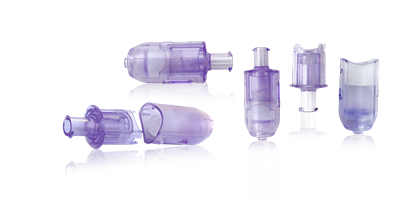

Interlinked AB has signed binding distributor agreements with minimum volume commitments across Europe, the Middle East and North America, establishing a repeatable distributor-led commercial model for its patented ReLink/LinkUS safety connector platform. The CE‑MDR approved technology (FDA registered for drain) targets reduction of accidental catheter dislodgement, with North American focus on LinkUS Drain for nephrostomy care; near-term priorities include commercial rollout, territorial expansion and securing growth capital to fulfill contracted orders. The deals materially advance international commercialization but will require additional funding and execution to translate into revenue.

Market structure: Interlinked’s distributor-led contracts with minimum volumes de-risk commercial execution and shift go-to-market costs onto partners; winners are distributors (scale players) and OEM catheter manufacturers that can bundle safety connectors, losers are low-cost reinsertion service capture (providers absorbing cost). Competitive dynamics favour firms able to integrate or acquire niche safety-IP quickly — expect modest pricing power for patented connectors but limited hospital willingness to pay without demonstrable net-cost savings. Cross-asset: modest positive credit sentiment for large distributors (MCK/CAH) and idiosyncratic upside for small med‑tech names; systemic FX/commodity impact negligible. Risk assessment: Immediate (days) market impact is minimal; short-term (60–180 days) risk centers on fulfillment and clinical publications that drive adoption; long-term (12–36 months) hinges on reimbursement coding and FDA indication expansion. Tail risks: failed funding round causing order-fulfillment collapse, product liability suits, or patent challenges that could dilute value or force recall. Hidden dependencies include hospital procurement cycles (quarterly budgets), imaging/IR workflow inertia, and distributor balance-sheet capacity to pre-finance inventory. Key catalysts: US publications (60–180 days), FDA clearance extension (6–18 months), announced distributor revenue recognition (next 90 days). Trade implications: Favor exposure to large diversified distributors and med‑tech acquirers and hedge small‑cap med‑tech tail risk. Use concentrated, time‑boxed positions (1–2%) in public distributors and targeted small med‑techs that could buy the IP; buy protective downside on med‑tech ETFs while selectively long acquisition candidates. Entry window: start scaling into positions after first US publication or within 90 days of verified distributor shipment; take profits on 12‑month +15–30% moves or cut at 12% loss. Contrarian angles: Consensus likely undervalues dilution/fulfilment risk — minimum-volume contracts reduce commercial risk but increase cash strain on Interlinked; if growth capital terms are dilutive, upside to early investors compresses. Historical parallels (needleless connector adoption) show slow hospital uptake until payors recognize net savings; absent reimbursement change, adoption may plateau. Unintended consequence: distributors could white‑label the tech or demand margin concessions, capping Interlinked’s long‑term unit economics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45