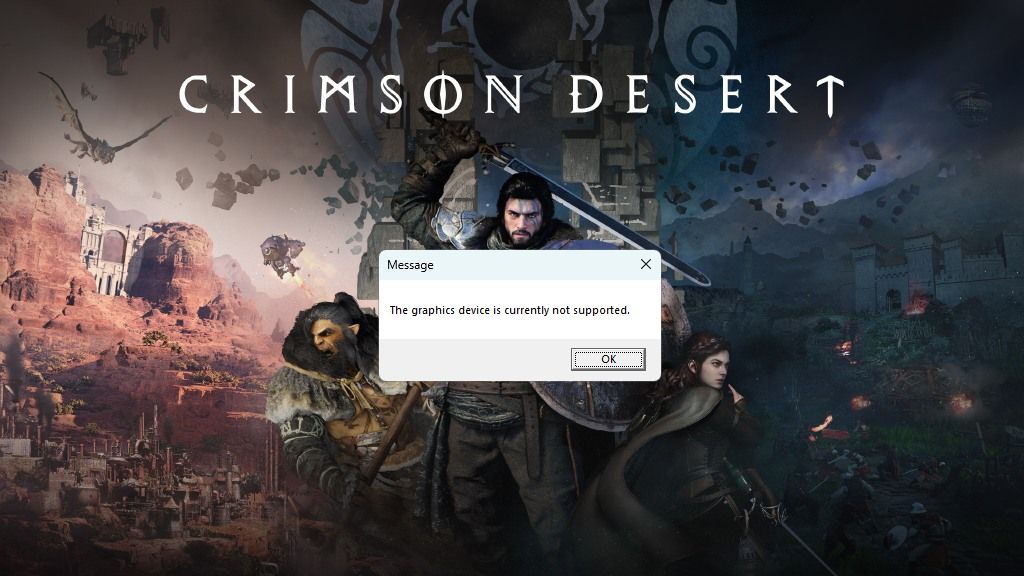

Crimson Desert launched without support for Intel Arc GPUs, with the game's FAQ advising affected players to seek refunds; Steam threads show similar 'graphics device not supported' errors across multiple GPU vendors. Intel says it reached out to Pearl Abyss 'many times' and provided early hardware, drivers, and engineering resources across multiple generations, while Pearl Abyss appears to have chosen not to enable Intel support at launch. The issue is unlikely to move markets materially given Intel's ~1% discrete AIB share per JPR, but it could harm consumer sentiment among laptop users with Arc GPUs and raise competitive/partnership frictions between developers and chip vendors.

This is primarily a developer-OEM engineering coordination failure with outsized signalling effects: studios that gatekeep launch compatibility create a negative feedback loop where marginal GPU vendors (or new architectures) suffer both perception and real-world testing deficits, accelerating a winner-takes-most optimization cycle that favors incumbents who already capture the majority of GPU dev mindshare. Over the next 1–6 months expect more dev resource prioritization toward the incumbents because each patch costs engineering hours; that raises effective marginal cost for supporting smaller vendors and increases the likelihood that support is delayed until an economic trigger (paid engineering, marketing co-op, or OEM pressure) arrives.

Market mechanics: this story is low-dollar but high-visibility — it matters for channel conversations and OEM marketing bundles rather than semiconductor supply constraints, so the direct revenue impact to chip fabs in the next quarter is minimal, while reputation and OEM negotiation leverage are the primary transmission channels. If Intel responds with funded engineering programs or expedited driver updates within days-weeks, the reputational hit is recoverable; if support requires multi-month engine changes or studio policy shifts, it will materially raise go-to-market costs for Arc and could slow OEM promotional cadence into the next laptop refresh cycle.

Broader second-order winners include middleware, engine-porting houses, and cloud/streaming providers that reduce per-device QA burden — a structural shift to more platform-agnostic graphics stacks would erode single-vendor optimization rents over 1–3 years. Key catalysts to watch are (a) driver release notes and validated game patches in the next 0–90 days, (b) any announced Intel studio engineering agreements or co-funding, and (c) OEM marketing pull-through on upcoming laptop SKUs; these determine whether this remains a short PR cycle or a durable competitive headwind.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

-0.05

Ticker Sentiment