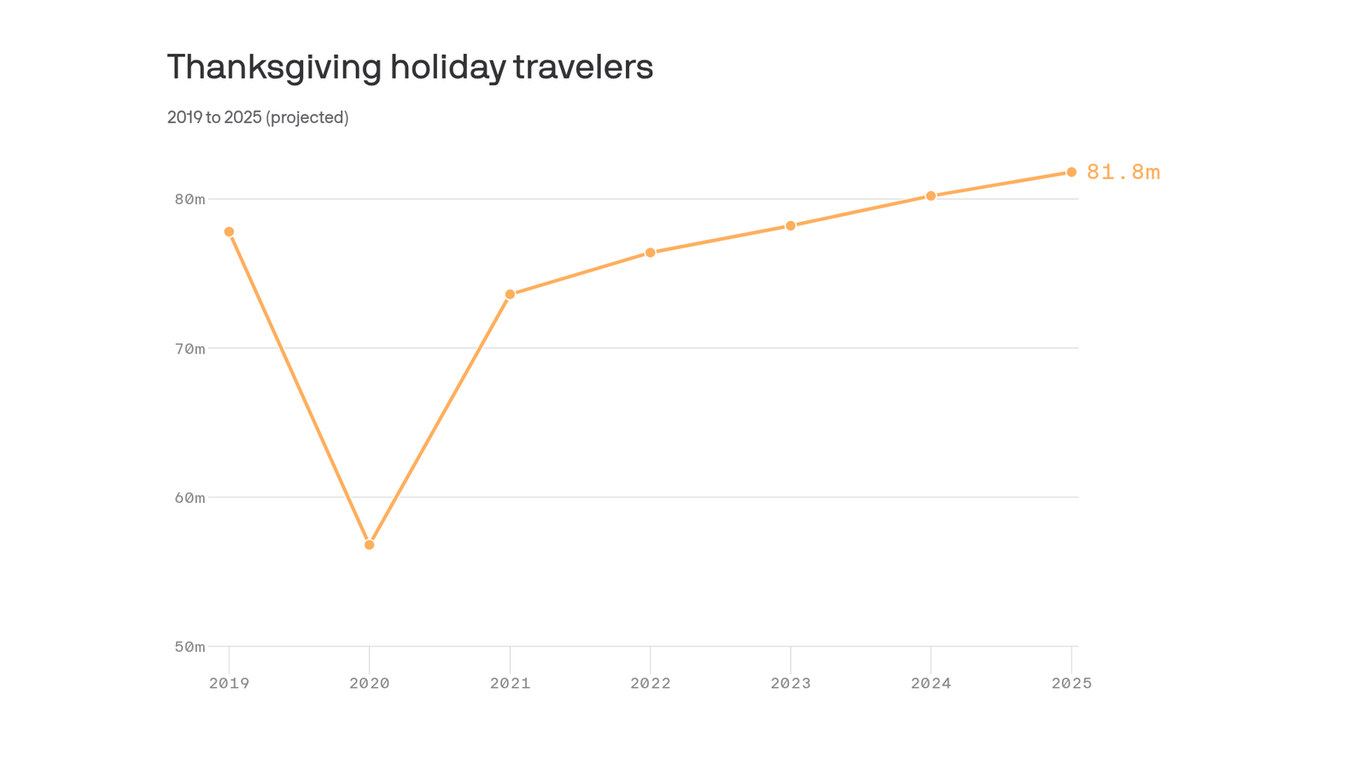

AAA projects 81.8 million Americans will travel at least 50 miles between Nov. 25 and Dec. 1, with 73 million (90%) by car and nearly 2.5 million using bus, train or cruise (+8.5%). AAA forecasts 6 million air travelers but the TSA expects to screen more than 17.8 million people over the period (including over 3 million on the Sunday after Thanksgiving), while Amtrak has seen nearly double-digit early booking growth year-over-year following shutdown-related airport delays; average gasoline is $3.069/gal (vs. $3.056 in 2024). A forecasted colder-than-normal Thanksgiving, with snow risk in parts of the Rockies and Interior Northeast, plus heightened TSA volumes, increases the risk of travel disruptions that could affect carriers, transit operators and near-term fuel demand.

Market structure: The 81.8M Thanksgiving travelers and 73M car travelers (90%) shift immediate demand toward rental cars (CAR, HTZ), aftermarket/parts retailers (ORLY, AAP) and ground-transport operators, while airlines (AAL, UAL, DAL, LUV) face concentrated operational risk and potential revenue dilution from delays/cancellations. Bus/train/cruise up 8.5% to ~2.5M signals modest modal share gains for rail/cruise players but not a structural collapse of air travel; gas demand moves are marginal (avg $3.069/gal vs $3.056 in 2024) but localized heating/fuel spikes possible in cold pockets. Risk assessment: Primary tail risks are a major weather event or systemic airport staffing failure that creates multi-day cancellations (>$200mm aggregate airline revenue shock across a few carriers) and legal/regulatory backlash on refunds/compensation. Immediate window: days (holiday travel); short-term: weeks (post-holiday operational/earnings prints); long-term: quarters if consumers permanently shift modes — hidden dependencies include parcel/logistics stress (UPS, FDX) and used-car market dynamics from rental fleet churn. Trade implications: Tactical overweight rental car equities and auto-aftermarket retailers for a 1–3 month hold while short selective airlines via put buys or short stock to capture operational risk; sell calendar or vertical call spreads on airlines if IV spikes. Rotate +2–4% portfolio weight from large-cap airline exposure into autos/consumer discretionary names tied to ground travel; enter 48–72 hours before peak travel and trim into any news-driven recovery within 2–6 weeks. Contrarian angles: The market may over-penalize airlines for a transient shock — if no major storms occur, expect a quick rebound similar to 2018 winter disruption patterns, making short-dated puts expensive and mean-reversion trades attractive. Also, stronger car travel can tighten rental fleet availability and support CAR/HTZ pricing for several quarters; consider selling short-term volatility after IV spikes rather than holding directional airline shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00