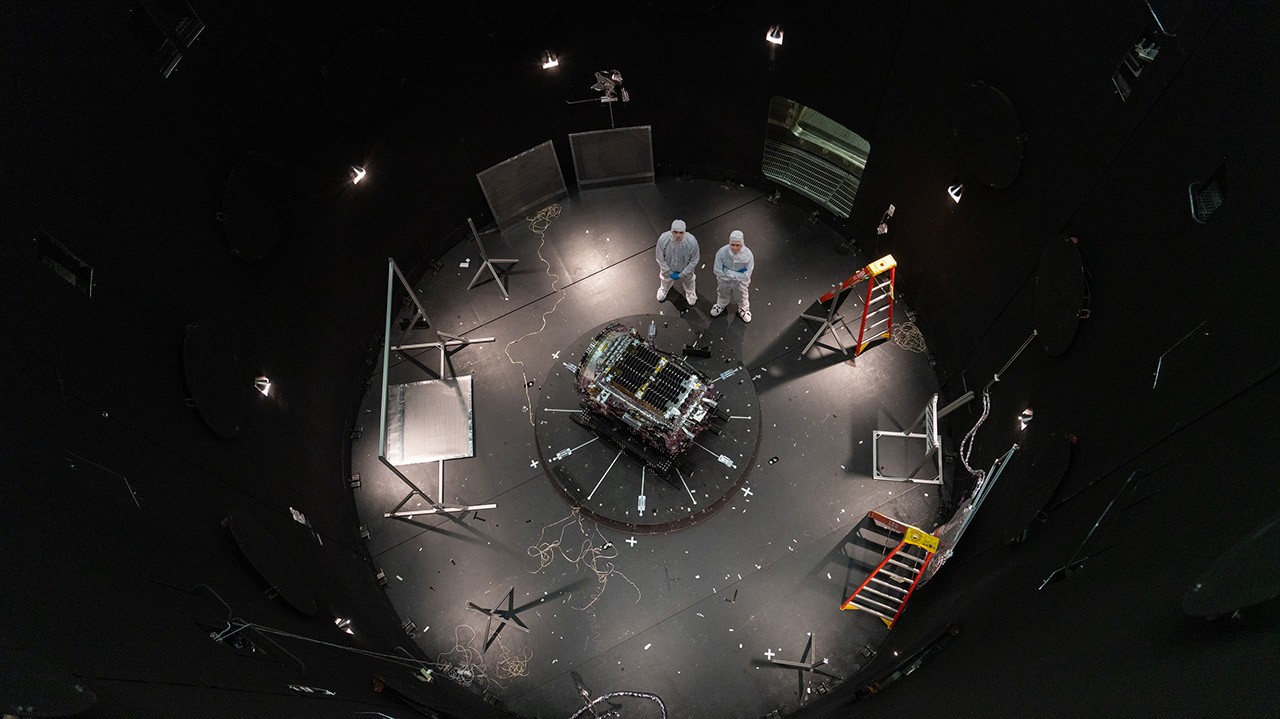

Katalyst completed environmental testing of its LINK robotic servicing spacecraft at NASA Goddard ahead of a planned June launch to boost the orbit of NASA’s Neil Gehrels Swift Observatory. The mission remains high-risk and time-sensitive, with Swift expected to re-enter the atmosphere later this year if the orbit raise is not attempted. Northrop Grumman is set to integrate LINK into a Pegasus rocket in early June, with launch later that month.

This is less a pure space headline than a proof point for a new micro-market in on-orbit servicing. If the mission works, it de-risks a class of “extend life / reposition / salvage” offerings that could become a meaningful niche for primes and specialty integrators, with the real economic upside coming from avoiding replacement capex rather than from the servicing fee itself. That dynamic favors firms with flight heritage, launch access, and rapid mission iteration; it also raises the bar for competitors that have technology but lack a credible execution track record.

The second-order beneficiary is Northrop Grumman’s small-launch and integration franchise: this is the kind of mission where schedule certainty and spacecraft handling matter more than raw payload economics. Even if the dollar value is modest, a successful Pegasus-linked execution would reinforce Northrop’s “mission-enabling infrastructure” positioning and support future government and commercial tasking around urgent orbital interventions. The risk is that a single high-visibility failure would not just kill one mission; it could slow procurement willingness for years because the buyer’s problem is existential, not discretionary.

From a timing standpoint, the near-term catalyst window is binary over the next 4-8 weeks, with much of the reputational impact realized on launch and rendezvous milestones rather than on final orbit-raising success alone. The contrarian angle is that the market may underappreciate how much schedule compression is itself a positive signal: teams that can close testing, integration, and launch prep in months rather than years can capture a first-mover advantage in a sector where certification cycles typically inhibit newcomers. That said, because the addressable revenue pool is still small, any enthusiasm should be treated as an option on a broader servicing ecosystem rather than as a standalone earnings driver.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.15

Ticker Sentiment