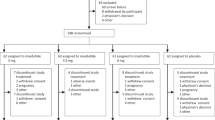

A phase 3 randomized trial in 320 Chinese adults with type 2 diabetes showed the dual GCGR/GLP-1R agonist mazdutide produced statistically robust glycaemic and weight-loss benefits at 24 weeks versus placebo: HbA1c reductions of -1.57% (4 mg) and -2.15% (6 mg) versus -0.14% for placebo (treatment differences -1.43% and -2.02%, both p<0.0001), and weight changes of -5.61% (4 mg) and -7.81% (6 mg) versus -1.26% for placebo (p<0.0001). Adverse events were typical of GLP‑1 receptor agonists (diarrhoea, decreased appetite, nausea); results materially strengthen the case for regulatory approval and commercial rollout in China and support broader market potential in T2D/obesity therapeutics.

Market structure: Mazdutide’s phase‑3 data (HbA1c -1.57% to -2.15%, weight -5.6% to -7.8% at 24 weeks) validates dual‑agonist strategies and will benefit large-cap GLP‑1/next‑gen obesity leaders (e.g., NVO, LLY) via expanded clinical proof‑points while pressuring mono‑GLP‑1 pure‑plays and legacy diabetes drug margins in China. Payors and hospital procurement in China gain leverage to demand steeper discounts given rapid efficacy and short diabetes duration (mean 1.9y) of trial population, implying downward pricing pressure in tender markets within 6–18 months. Risk assessment: Near‑term (days–weeks) risk is market repricing on publication and headlines; short‑term (3–12 months) risks include regulatory pushback, safety signals (hepatic or CV class effects), and national price controls in China; long‑term (1–5 years) risk is capacity/CMC bottlenecks and rapid class commoditization driving gross‑to‑net erosion >300–500bps. Tail scenarios: regulatory safety hold or revealed adverse CV signal (low‑probability) would cause >30% re‑rating in small‑cap peers; conversely fast reimbursement in China could drive 10–20% upside for manufacturers with local scale. Trade implications: Tactical: favor scalable, diversified leaders—construct limited-duration bullish option structures on NVO and LLY (6–9 month call spreads) to capture class re‑rating with capped capital; trim speculative small‑cap biotech and XBI exposure (rotate 1–3% into IBB/XBI hedges). Cross‑asset: expect modest downward pressure on Chinese pharma high‑yield bonds and slight strengthening of RMB if domestic launches cut import demand; increase hedges on biotech volatility (buy put spreads on XBI). Contrarian angles: Consensus may overstate immediate commercial impact—China price caps, payer step edits, and manufacturing scale will delay broad uptake 6–18 months, leaving a window where large incumbents can defend share. Historical parallel: initial GLP‑1 efficacy hype (post‑Ozempic) led to overshoot in small‑cap valuations then consolidation; look for overpriced pure‑play dual‑agonist developers lacking phase‑3 breadth as short candidates.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55