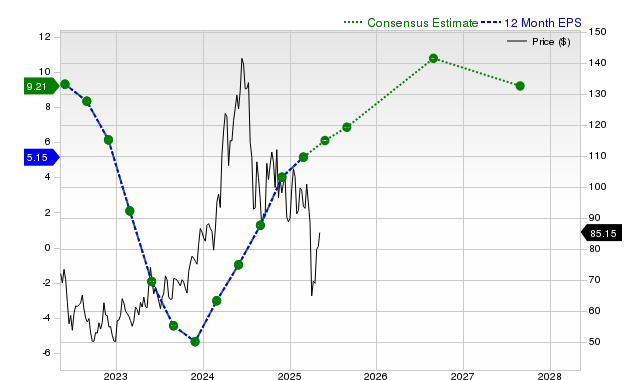

Micron Technology (MU) has recently underperformed the S&P 500 and its industry, yet its near-term prospects appear strong, driven by significant upward revisions to earnings and revenue estimates. Analysts project current quarter EPS to surge 112.7% year-over-year, with substantial growth also expected for current and next fiscal years. This positive momentum in estimates, coupled with a consistent history of beating consensus, has earned MU a Zacks Rank #2 (Buy), indicating potential near-term outperformance despite its current valuation being in line with peers.

Despite a recent 7.3% decline in share price over the past month, which significantly underperformed the S&P 500's +5.9% gain, Micron Technology's (MU) forward-looking fundamental indicators appear exceptionally strong. The primary driver for this optimistic outlook is the substantial upward revision of earnings estimates by sell-side analysts. The consensus EPS estimate for the current quarter has increased by 24.1% over the last 30 days to $2.51, representing a projected 112.7% year-over-year growth. This momentum extends through the fiscal year, with consensus estimates pointing to 497.7% EPS growth for the current year and a further 57.9% for the next, supported by revenue growth forecasts of +46.5% and +32.9% for the same periods, respectively. This positive revision trend is bolstered by a strong history of execution, where Micron has beaten consensus EPS estimates in each of the last four quarters, including a +20.13% surprise in its most recent report. While its valuation is considered neutral and at par with peers (Zacks Value Grade 'C'), the strength and magnitude of the earnings revisions have resulted in a Zacks Rank #2 (Buy), suggesting the fundamental picture may signal near-term outperformance.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment