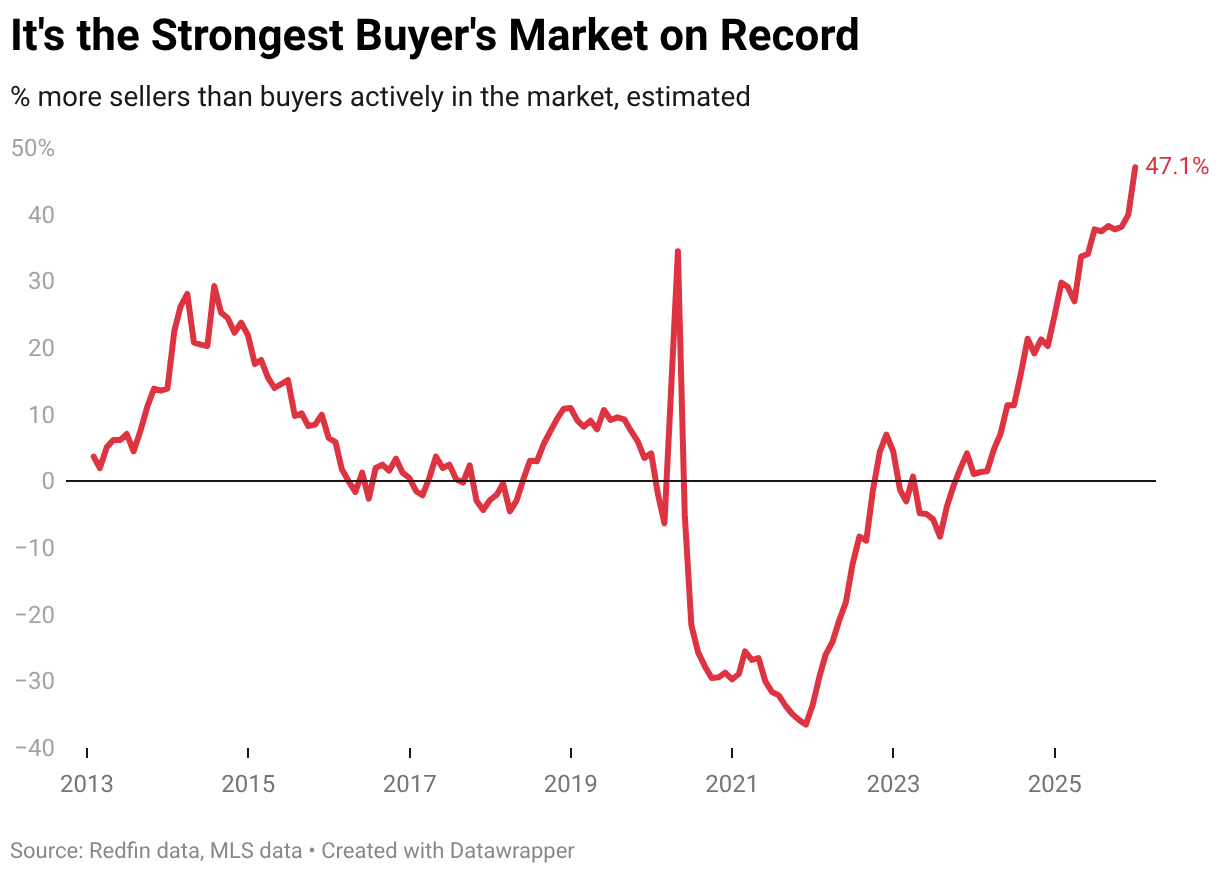

U.S. housing supply far outstripped demand in December, with an estimated 47.1% more sellers than buyers (about 631,535 more), the largest gap on record back to 2013 and the biggest monthly increase since Sept. 2022. Redfin estimates buyers fell to ~1.34M (down 5.9% month-over-month and 11.8% year-over-year) while sellers were ~1.97M (down 1.1% MoM, up 3.9% YoY); 36 of the 50 largest metros were buyer’s markets. Local weakness is acute in Sun Belt metros (Austin +128% sellers over buyers; Dallas +86.8% with Dallas median price down 7.6% YoY), national median prices rose just 0.1% in December, and recent slight drops in mortgage rates could modestly affect buyer activity in January.

Market structure: The 47% excess of sellers signals a national buyer’s market driven by localized oversupply (Sun Belt) and demand destruction from high rates and affordability. Winners: cash-ready buyers, discount-focused brokers, and long-duration bonds; Losers: speculative homebuilders, regional MLS-dependent brokers, and mortgage credit-sensitive lenders in high-inventory metros (Dallas, Austin, Miami). Expect continued downward price pressure in high-build metros (Dallas -7.6% Y/Y as an early indicator) while Northeast/Midwest pockets preserve pricing power. Risk assessment: Tail risks include a >10% localized price collapse if new completions continue at current pace and unemployment ticks up 100–200 bps, forcing distressed sales and bank CRE re-pricing. Immediate catalysts (days–weeks) are mortgage-rate moves: a sustained fall below ~5.75–6.00% could materially revive demand; conversely Fed hawkishness or job shocks over months could deepen the buyer advantage. Hidden dependencies: insurance/HOA cost shocks (Florida) and regional migration reversals which can amplify imbalances. Trade implications: Favor defensive duration and trades that short construction/exposure to new supply while hedging MBS convexity; expect MBS spreads to widen and 10y Treasuries to outperform if housing meaningfully softens. Use concentrated option hedges to control risk (3–6 month expiries), and rotate out of cyclical housing supply chain names into defensive REITs in seller markets (Northeast) and consumer staples/utilities. Contrarian angles: Consensus underestimates how quickly affordability-led price weakness can convert to demand once mortgage rates fall — a 50 bps drop in 10y yields historically lifts transactions by ~10–20% seasonally. Shorting homebuilders indiscriminately is risky: well-capitalized builders with low land exposure (PHM vs DHI) may be mispriced. Unintended consequence: sharp price declines could restore affordability and produce a snap-back in 6–12 months, creating a compelling long-entry window in building materials and home-improvement retail.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35