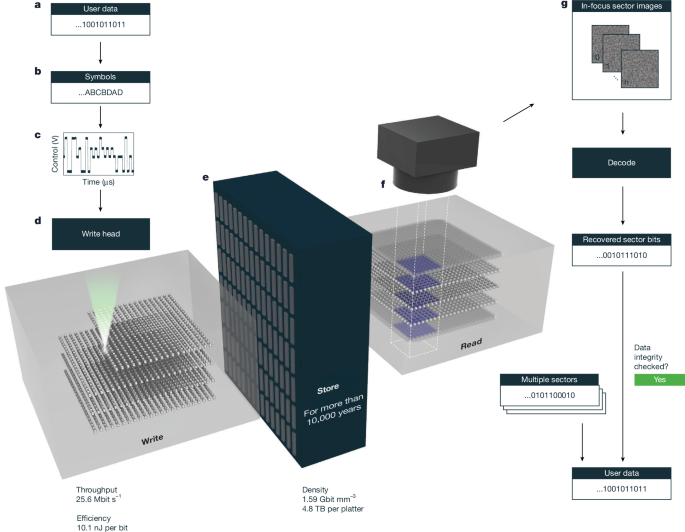

Microsoft Research’s Project Silica demonstrates an end-to-end optical archival storage system using femtosecond laser writing in glass, achieving up to 1.59 Gbit mm−3 (4.84 TB usable per 120 mm × 120 mm × 2 mm platter) with birefringent voxels and 0.678 Gbit mm−3 (2.02 TB) with phase voxels. Key performance figures include single-beam write throughputs of 25.6 Mbit/s (birefringent) and 18.4 Mbit/s (phase), multibeam throughput scaled to 65.9 Mbit/s with four beams, energy efficiencies ~8.85–10.1 nJ/bit, machine-learning decoding with LDPC FEC, and accelerated-aging projections indicating data lifetimes >10,000 years; several related patents have been filed by Microsoft. The result signals a potential long-duration, low-maintenance archival medium that could affect cloud archival economics and suppliers of cold-storage infrastructure over the medium term.

Market structure: Microsoft (MSFT) is the clear strategic winner—it owns IP, cloud integration capabilities and can internalize licensing and service revenue if Project Silica commercializes; precision optics/laser suppliers (NOVT, COHR) are second‑order beneficiaries from capex for writers/readers. Legacy archival vendors (tape/HDD) face gradual pricing/volume pressure over years, not months: expect meaningful share shifts only if per‑TB cost and automation parity are reached (~3–7 years). Demand signal: near‑term spike in orders for femtosecond lasers, polygon scanners and high‑NA optics; throughput scaling (10→50+ MHz lasers, or 4× beams) implies supplier revenue upside of potentially several hundred million annually if cloud rollouts occur. Risk assessment: key tail risks include IP litigation or exclusivity (MSFT patents), export controls on high‑power femtosecond lasers, and operational scaling failures (multi‑beam thermal limits). Time horizons: immediate (days–weeks) = PR/vol spikes; short (3–12 months) = supplier order flow/partnership announcements; long (2–5 years) = actual substitution of tape/HDD for cold archives. Hidden dependencies: robotic handling, LDPC/ML decode integration, camera FOV/cost; a single bottleneck (laser supply constrained) could delay commercialization by >12 months. Catalysts: MSFT product launch, vendor supply agreements, major cloud provider pilot wins. Trade implications: tactically favor MSFT long (IP + cloud monetization) and select optics/laser suppliers (NOVT, COHR) for 6–18 month plays tied to order reports. Pair idea: long NOVT vs short legacy HDD (STX/WDC) to express component demand vs media decline. Options: buy 9–15 month LEAPS or call spreads on MSFT to capture asymmetric upside from commercialization; buy 6–9 month OTM calls on NOVT/COHR ahead of expected trade show/order cycles. Rotate modest weight from pure storage (HDD/tape) into photonics, industrial automation and cloud infrastructure names over next 6–24 months. Contrarian angles: consensus understates commercialization friction—histor parallels (optical formats, 3D NAND adoption curves) show multi‑year ramp and niche initial penetration; optics suppliers may be over‑priced on PR alone. Watch metrics: if NOVT/COHR rally >20% without confirmed multi‑M$ purchase orders within 90 days, treat as overbought and trim. Unintended consequences: persistent long‑term immutable archives could trigger stricter data‑retention/privacy regulation, raising compliance costs for cloud vendors and slowing uptake.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment