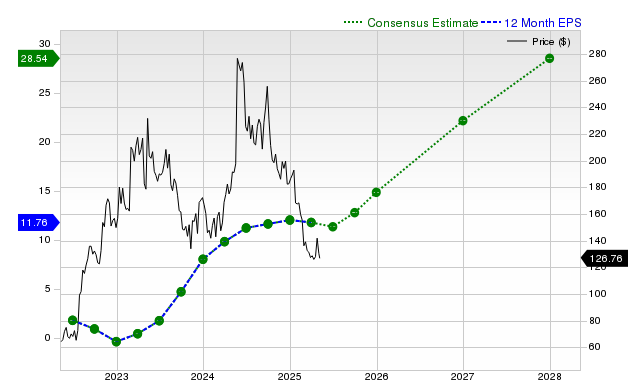

First Solar (FSLR) is attracting significant investor attention, despite its shares declining 2.7% over the past month against broader market and industry gains. Analysts project robust future growth, with current fiscal year EPS estimated to rise 26.2% and next fiscal year EPS by 52.3%, complemented by substantial revenue growth forecasts of 27.6% and 16% respectively. However, the stock holds a Zacks Rank #3 (Hold), indicating an expectation of in-line performance with the broader market in the near term, and a 'C' grade on its Zacks Value Style Score suggests it trades at par with peers.

First Solar (FSLR) presents a dichotomous profile, characterized by strong forward-looking fundamentals juxtaposed with recent market underperformance. Despite significant investor interest, the stock has declined 2.7% over the past month, lagging both the S&P 500's 2.6% gain and, more notably, its own Zacks Solar industry's 7.4% rise. This performance disconnect contrasts sharply with robust analyst estimates, which project substantial growth. For the current fiscal year, consensus EPS is forecast to increase by 26.2%, accelerating to 52.3% in the next fiscal year. This is supported by revenue growth projections of 27.6% and 16% for the current and next fiscal years, respectively, with a particularly strong current quarter forecast of +74.2% year-over-year revenue growth. However, tempering this outlook is the company's inconsistent surprise history, having surpassed EPS estimates only once in the last four quarters. Furthermore, the stock carries a Zacks Rank #3 (Hold), suggesting it is expected to perform in line with the broader market in the near term, and its 'C' grade for value indicates it is trading at par with its peers, offering no clear valuation discount.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment