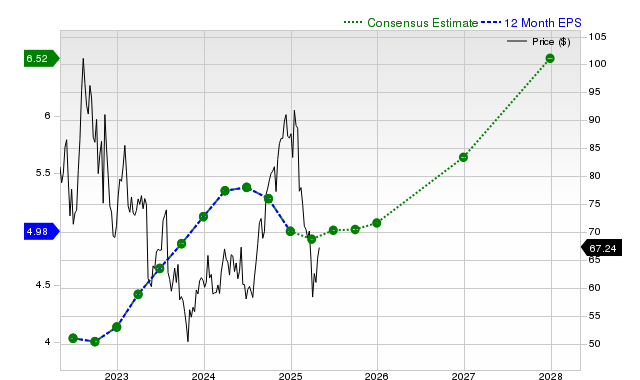

PayPal (PYPL) has received a Zacks Rank #2 (Buy), indicating potential near-term market outperformance. Despite its shares returning +4.8% over the past month, slightly trailing the S&P 500's +5.2%, it significantly outperformed its industry, which declined by 1.5%. The digital payments firm is projected to achieve strong earnings growth, with current quarter EPS estimated at $1.29 (+8.4% YoY) and full-year EPS at $5.08 (+9.3% YoY). Furthermore, PayPal's valuation, reflected by a Zacks Value Style Score of 'B', suggests it is currently trading at a discount relative to its peers.

PayPal Holdings (PYPL) presents a narrative of strong projected profitability and attractive valuation juxtaposed with tepid revenue growth. The stock's +4.8% gain over the past month has significantly outpaced its Financial Transaction Services industry (-1.5%) but slightly lagged the S&P 500 composite (+5.2%), indicating a company-specific story is unfolding. The primary bull case rests on consensus earnings estimates, which project robust year-over-year EPS growth of +8.4% for the current quarter and +9.3% for the current fiscal year, accelerating to +11.2% for the next fiscal year. This is supported by a strong history of beating EPS consensus for four consecutive quarters, including a +15.65% surprise in the last report. Furthermore, a Zacks Value Style Score of 'B' suggests the stock is trading at a discount to its peers. However, this is tempered by a weak top-line performance. The last reported quarter saw revenue grow only +1.2% YoY, missing estimates, and projections remain modest at +2.5% for the current quarter and +3% for the fiscal year. Critically, despite the positive outlook, analyst earnings estimates have remained unchanged over the last 30 days, suggesting a lack of fresh upward catalysts to drive revisions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.65

Ticker Sentiment