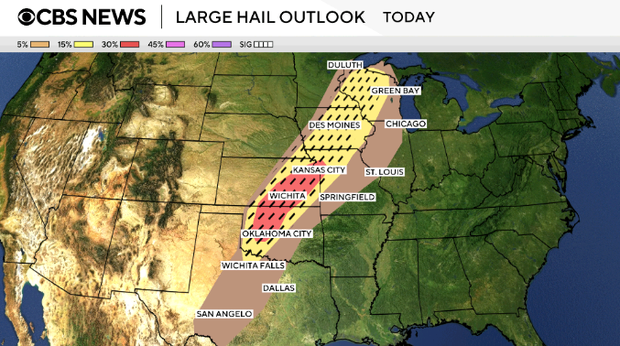

More than 51 million people are under severe weather threat Friday evening, with forecasts calling for strong tornadoes, very large hail, damaging winds up to 70 mph, and flash flooding across the central U.S. The article highlights ongoing cleanup from earlier tornadoes in New York and Missouri, plus record flooding in Michigan where 33 counties are under a state of emergency. This is a broad regional disruption with potential to affect transportation, property, utilities, and local economic activity into the weekend.

The immediate equity impact is less about a broad macro shock and more about which balance sheets absorb localized repetition: utilities, construction, retail logistics, and regional insurers are the first-order exposure set, but the second-order winner is the large-cap infrastructure replacement complex. The sequence of storm, flood, and cleanup events raises the odds of a multi-week claims and repair cycle, which tends to favor distributors of roofing, drywall, electrical, and heavy equipment over the original local contractors who face labor bottlenecks and margin leakage.

For insurers and reinsurers, the key issue is not headline catastrophe size but frequency clustering across adjacent states. A few medium-sized events compress underwriting margins faster than one-off disasters because reinsurance attachment points are hit repeatedly and loss-adjustment expenses rise with every event; that can pressure regional P&C multiples for 1-2 quarters even if the ultimate loss ratio does not look catastrophic. The better relative expression is to prefer firms with diversified geographies and higher commercial lines mix over small-cap homeowners carriers concentrated in the Midwest.

The infrastructure angle is more durable: flood remediation, road repair, power restoration, and school/public building cleanup often convert into incremental spend over 30-90 days, with some effect persisting into the next budget cycle. The contrarian miss is that this is not automatically bullish for every “rebuild” name; if storms continue into the weekend, the near-term effect is working-capital strain, project delays, and labor scarcity before revenue recognition catches up. That argues for trading the setup as a volatility event first, not a straight-line beneficiaries basket.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

A final second-order risk is transport and inventory disruption across the Upper Midwest corridor, which can create temporary outperformance in expedited freight and selective industrials with disaster-response exposure. If flooding persists, expect localized commodity basis dislocations and higher spot pricing for materials, but the trade window is short unless weather remains active into the next 2-3 weeks. In other words, the market may underprice how quickly repeated severe-weather clusters migrate from a sympathy trade into an actual earnings revision cycle for insurers and regional consumer names.