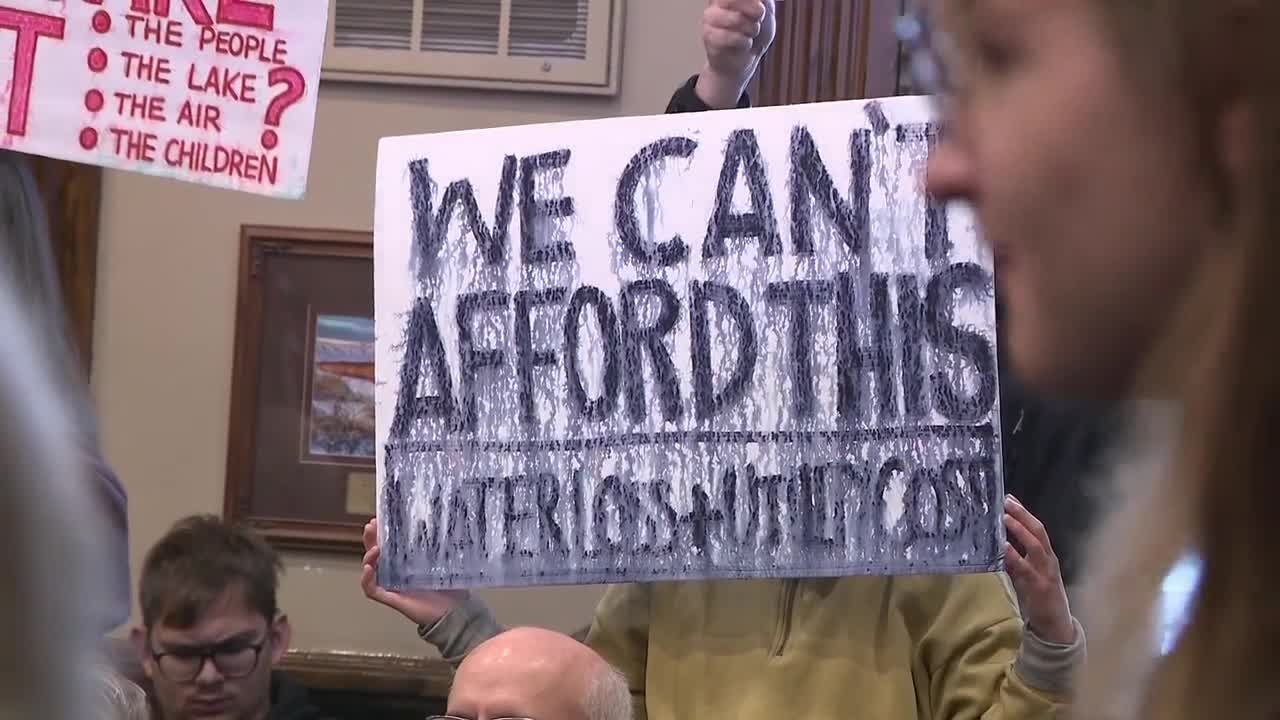

Box Elder County commissioners tabled a vote on a planned 40,000-acre AI data center in Utah, delaying final approval amid resident concerns over water use, secrecy, and rushed decision-making. MIDA said the project could eventually support up to 8 gigawatts of power, generate more than $100 million in annual county revenue, and create about 2,000 permanent jobs over a roughly 10-year buildout. However, officials also acknowledged no traffic or environmental impact studies had been completed, keeping the near-term outlook uncertain.

This is less about one data center and more about a new template for monetizing power, land, and permitting under a national-security wrapper. The key second-order effect is that if a project like this gets institutional backing, it raises the odds of similar greenfield AI-campus proposals in exurban areas where local opposition is fragmented but infrastructure is thin. That shifts the bottleneck from chips to transmission, gas peakers, water rights, and municipal consent, which should support the entire “picks-and-shovels” stack while making project timelines far more political than technological.

The near-term losers are local landowners and municipalities that have to absorb uncertainty without hard environmental or traffic studies; the bigger market losers are incumbent utilities and grid operators that may face stranded planning assumptions if private generation and closed-loop water systems bypass them. The real beneficiaries are firms with exposure to power equipment, switchgear, transformers, gas generation, and industrial EPC, because this kind of buildout requires multi-year procurement before any revenue is realized. If the full 8 GW concept survives, the supply chain pressure is meaningful: transformer lead times, interconnect queues, and natural gas infrastructure availability could become the true gating items, not capital.

The contrarian view is that the headline scale is probably overstating the investable near-term opportunity. Projects of this size tend to get cut, delayed, or rephased as permitting, water, and community resistance introduce 12-24 month slippage, and that usually compresses the market’s enthusiasm for adjacent names. Another underappreciated risk is that “defense” framing can attract scrutiny from state and federal regulators if tax abatements appear to subsidize private AI economics, which could slow approvals or trigger political backlash if the promised jobs prove less durable than advertised.

For trading, the cleanest expression is to stay long the infrastructure beneficiaries on dips while fading pure-play AI enthusiasm until the permitting path is clearer. This is a better medium-term catalyst for utilities and power equipment than for the data-center operator itself, because the first dollars get spent on substations, cables, cooling, and generation before the compute stack is fully monetized. The risk/reward favors a basket approach: upside from multi-year capex is visible, while the downside is mostly delay rather than cancellation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05