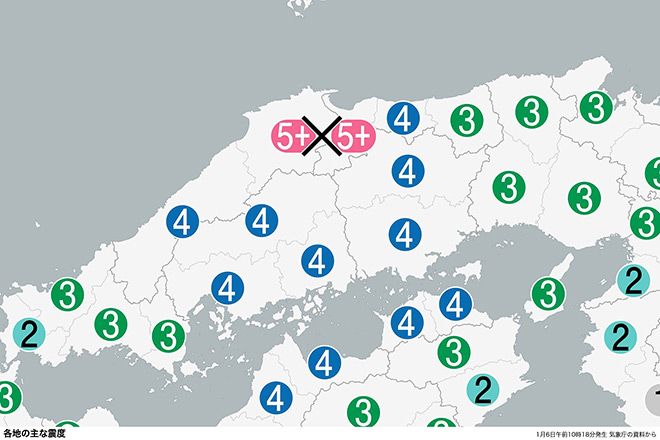

A magnitude-6.4 earthquake (depth ~11 km) struck eastern Shimane Prefecture at 10:18 a.m. JST on Jan. 6, producing a maximum seismic intensity of upper-5 on Japan's 7-point scale, causing several injuries, localized damage and ongoing aftershocks with warnings to remain vigilant for about a week. Transportation was disrupted — including a power outage and suspension on the Sanyo Shinkansen between Shin-Osaka and Hakata until ~1 p.m., regional rail suspensions and temporary expressway closures — while Chugoku Electric’s Shimane nuclear plant reported no abnormalities and its restarted No.2 reactor (820,000 kW) remained online, limiting immediate broader energy-market implications.

Market structure: Winners include domestic construction/engineering, heavy equipment and seismic-retrofit suppliers (demand lift concentrated over 3–12 months), regional logistics and temporary power contractors; losers are short-term travel/tourism operators, regional rail/expressway operators and local retailers where foot traffic drops. Expect a modest 1–3% revenue reallocation toward repair/retrofit budgets in affected prefectures over 6–12 months; pricing power rises for immediate-capacity contractors but margin pressure appears minimal for national firms. Risk assessment: Immediate tail risks include a larger (M≥7) aftershock within ~7 days (JMA warning) that could trigger material infrastructure damage or nuclear-containment scrutiny—low probability but high impact. Short-term (days–weeks) effects are operational (transport stoppages, power trips) and credit-lite; medium-term (weeks–months) regulatory risk centers on nuclear restarts and safety reviews which could delay regional utility earnings by ~1–3% and keep volatility elevated; long-term (quarters–years) is higher capex for retrofits and possible insurance/reinsurance rate repricing. Trade implications: Tactical cross-asset moves: JPY should behave as a modest safe-haven (potential 0.5–1.5% move vs USD intra-week); JGB yields likely to compress 5–15 bps if risk-off broadens. Use concentrated, short-duration hedges (1–3 week) rather than large directional equity bets; selectively go long domestic heavy-equipment/contractors for a 3–9 month recovery thesis while keeping hedges on broad Japan indices. Contrarian angles: Consensus will over-focus on immediate disruption; underpriced is demand for seismic-isolation and retrofitting specialist capex which can drive durable revenue for select midcaps over 6–18 months. Conversely, put-buying on Japan ETFs may be overpriced for >1 month tenors—favor calendar-limited protection (cheap spreads) rather than outright long-dated puts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30