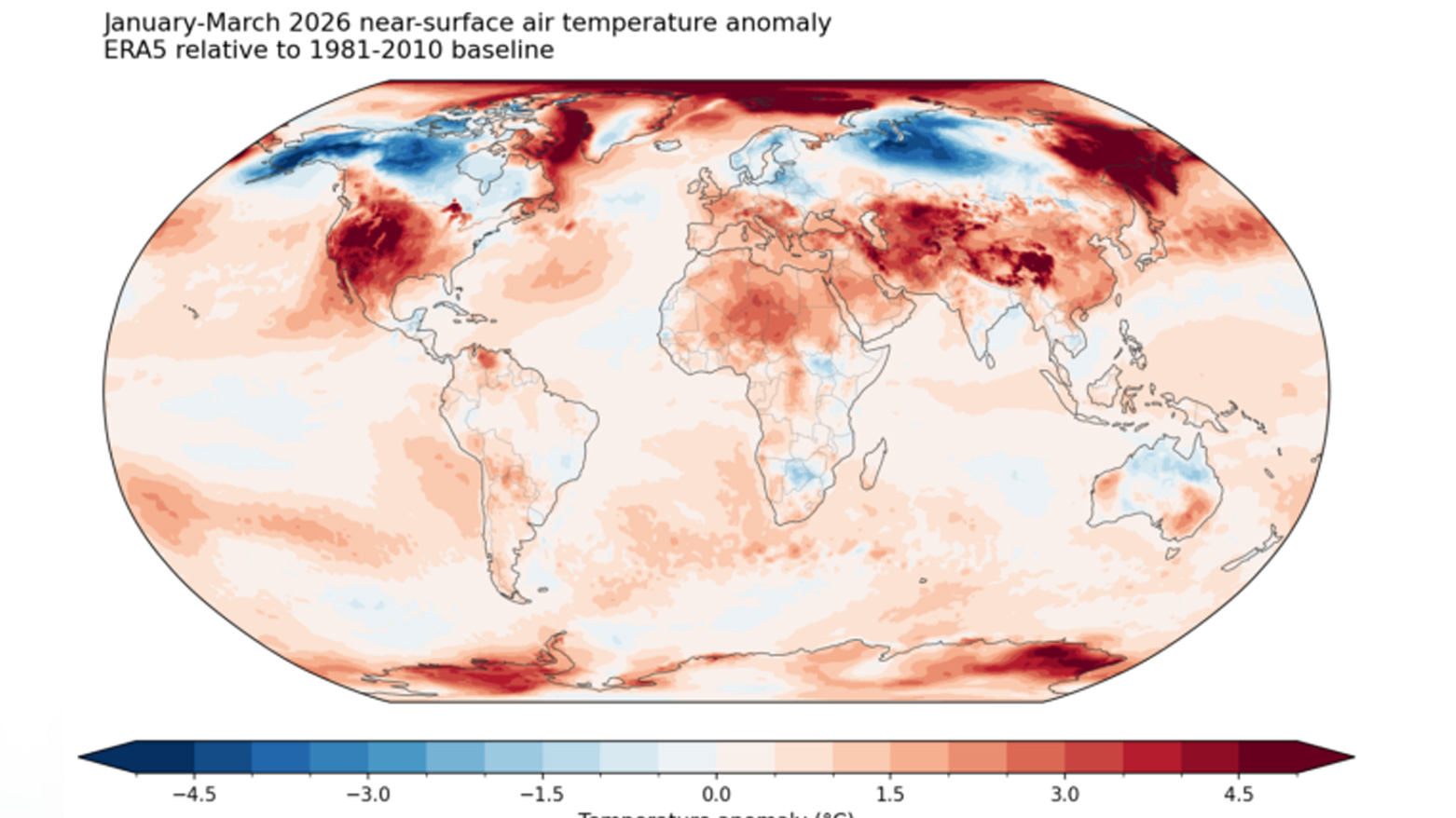

The UN’s WMO projects global temperatures will remain at or near record highs in 2026-2030, with an 86% chance at least one year exceeds 2024 as the warmest on record and a 75% chance the five-year average tops 1.5C above pre-industrial levels. The report also warns of accelerating Arctic warming and shifting precipitation patterns, reinforcing climate-risk concerns for agriculture, infrastructure, and energy planning. While largely a climate outlook rather than a direct market event, the findings are relevant for policy, ESG, and long-duration asset risk assessment.

The market implication is not a single “climate trade” but a widening dispersion trade across sectors with different weather pass-through. The most immediate beneficiaries are price-setters with low physical exposure and inflation linkage—utilities with regulated inflation escalators, insurance/reinsurance with hardening pricing, and select agribusiness/input names that can reprice faster than end-demand weakens. The losers are asset-heavy operators with fragile uptime economics: utilities with thermal generation, rail/logistics exposed to buckling/flood disruptions, and consumer staples/food producers whose margins get squeezed by crop volatility before they can fully pass costs through.

Second-order effects matter more than headline temperature levels. Repeated heat and precipitation anomalies tend to raise working capital needs, inventory buffers, and capex for redundancy; that is a quiet margin headwind for industrials, chemicals, and cold-chain logistics over the next 12–24 months. The more interesting trade is not “green good, fossil bad,” but “volatility up”: variability of harvests, power demand peaks, and insurance losses should lift earnings dispersion and justify higher option-implied vol in weather-sensitive baskets.

Catalyst timing is asymmetric. Near-term, the next heat dome or wildfire/flood episode can re-rate weather-exposed names within days; over 6–18 months, the bigger catalyst is policy and underwriting reset—higher premiums, tighter municipal/federal resilience spending, and accelerated adaptation capex. The contrarian miss is that chronic warming is not uniformly bearish for all carbon-intensive firms: firms with flexible pricing, asset rotation, and geographic diversification can monetize volatility, while the truly vulnerable are those with fixed tariffs, legacy infrastructure, and poor balance-sheet flexibility.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.20

The cleanest positioning is to lean into dispersion rather than direction. A long/short basket on insurers/reinsurers versus exposed utilities or transport names should outperform as loss-cost inflation compounds. On the upside, select climate-resilience and grid-hardening names should benefit from multi-year capex cycles, while on the downside the most fragile food producers and inland logistics operators look vulnerable to repeated weather shocks that markets still tend to treat as transitory.