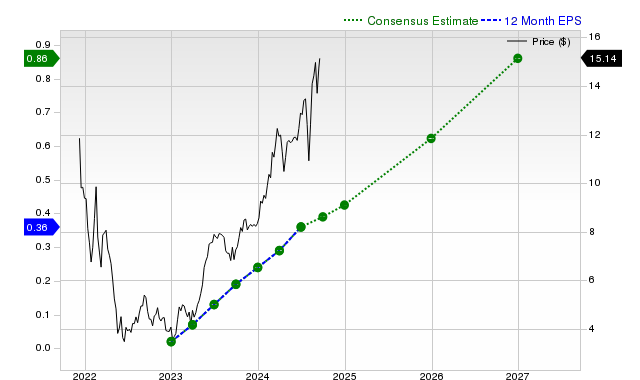

Nu Holdings (NU) has recently outperformed the S&P 500 and its industry, with shares gaining 12.3% in the past month. The company projects robust future earnings and revenue growth, with current fiscal year estimates up +20% and +29.4% respectively, though its latest reported quarterly revenue of $3.25 billion slightly missed consensus. Despite strong growth projections, Zacks maintains a 'Hold' (#3) rating, suggesting near-term market-in-line performance, and notes a valuation concern as NU trades at a premium to its peers.

Nu Holdings Ltd. (NU) presents a mixed profile characterized by strong forward-looking growth projections counterbalanced by a premium valuation and recent performance inconsistencies. The stock has demonstrated significant momentum, returning +12.3% over the past month and outperforming both the S&P 500 composite and its foreign banking peers. This performance is underpinned by robust consensus estimates, which project full-year revenue growth of +29.4% and EPS growth of +20%, accelerating to an expected +45.1% EPS increase next fiscal year. However, these bullish forecasts are tempered by recent results; in its last reported quarter, Nu missed revenue consensus by 2.52%, although its EPS of $0.12 met expectations. This execution risk is compounded by valuation concerns, as the company receives a 'D' grade on the Zacks Value Style Score, indicating it trades at a premium to its peers. The resulting Zacks Rank #3 (Hold) suggests that, despite the high growth outlook, the stock may perform in line with the broader market in the near term as investors weigh the growth narrative against the rich valuation and execution precedents.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

Neutral

Sentiment Score

0.00

Ticker Sentiment