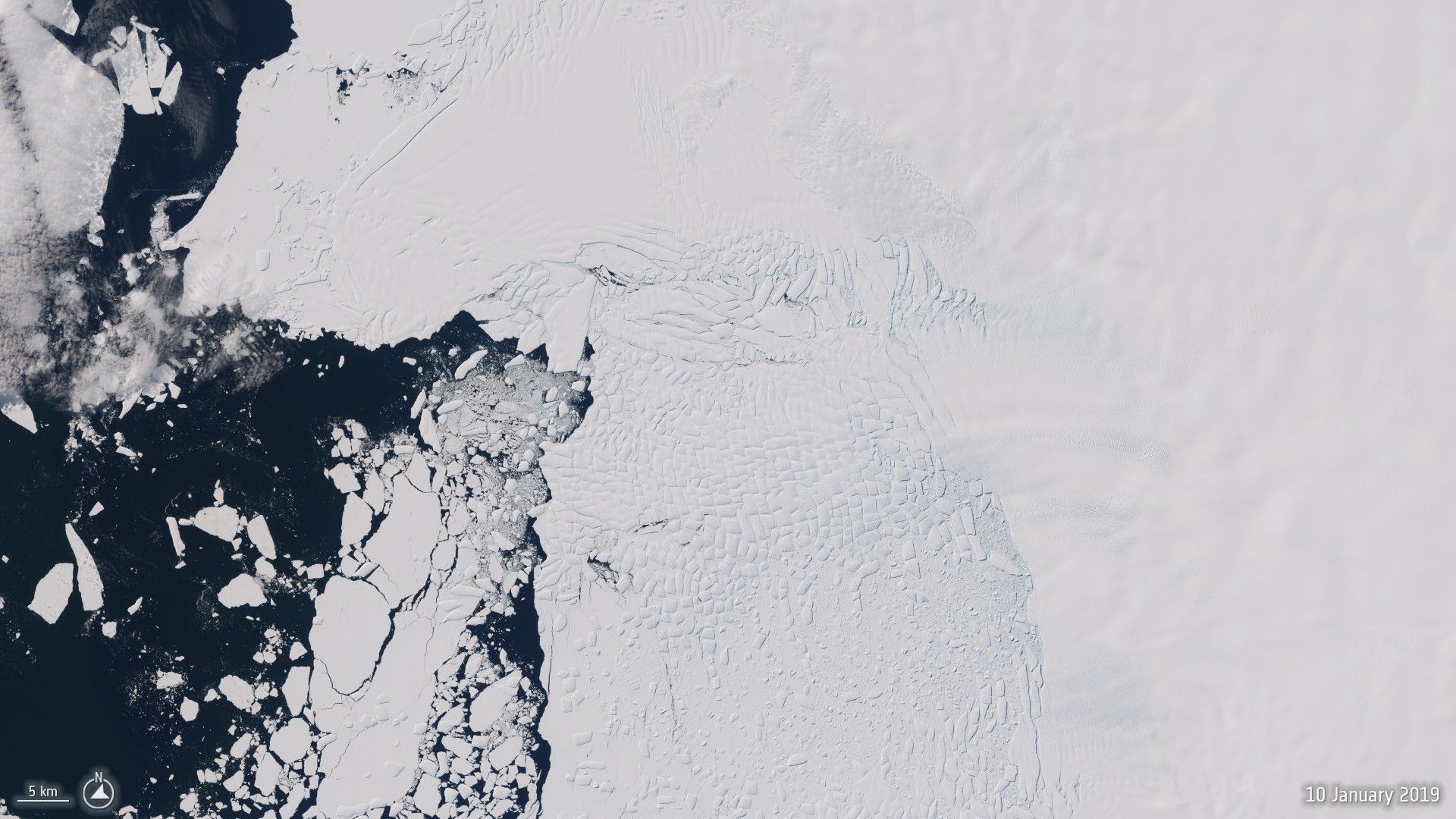

Thwaites Glacier is expected to lose its eastern ice shelf this year, a development researchers say will accelerate ice loss and could ultimately contribute 65 cm (26 inches) to global sea levels. The article warns that eventual collapse of the glacier would worsen long-term coastal flooding risks for major cities and could destabilize additional West Antarctic Ice Sheet glaciers, implying more than 3 meters of potential sea-level commitment over the very long term. The near-term event is scientific rather than directly market-driven, but it reinforces material climate-risk implications for infrastructure, insurance, and coastal real estate.

The market is likely underpricing the difference between a headline climate event and a tradable acceleration in liability. The near-term catalyst is not catastrophic sea-level rise but a higher-probability step-up in the perceived pace of coastal risk, which tends to reprice municipal credit, flood insurance, and long-dated infrastructure maintenance budgets before it shows up in macro data. That means the first-order winners are not “climate” equities per se, but firms with pricing power over adaptation spend: coastal engineering, water infrastructure, and specialty reinsurers with sophisticated cat models.

The second-order effect is a slow, persistent widening in the cost of capital for the most exposed geographies. Municipalities and quasi-sovereigns in low-lying metros may face a gradual divergence in spreads versus inland peers as investors begin to discount not just storm frequency but the probability of chronic nuisance flooding becoming a budget line item. That creates a durable relative-value setup in credit rather than a one-shot disaster trade, and it likely plays out over quarters to years, not days.

The bigger contrarian point is that the market may be too focused on the eventual sea-level endpoint and not enough on the policy response lag. Even if physical change is slow, budget authorities often delay capex until after repeated threshold events, then rush into multi-year retrofit cycles; that creates lumpiness in order flow for construction, pumps, drainage, levees, and coastal hardening. Conversely, the broad “renewables win, everything else loses” framing is too simplistic here — the trade is really about adaptation, insurance repricing, and municipal finance dispersion.

Tail risk is political: a single severe flooding season or a high-visibility scientific update can accelerate funding and disclosure requirements, pulling forward market recognition by 6-18 months. If ocean circulation dynamics or model uncertainty soften the narrative, the trade should still work because the investment cycle is driven by perception of risk, not just realization of it.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75