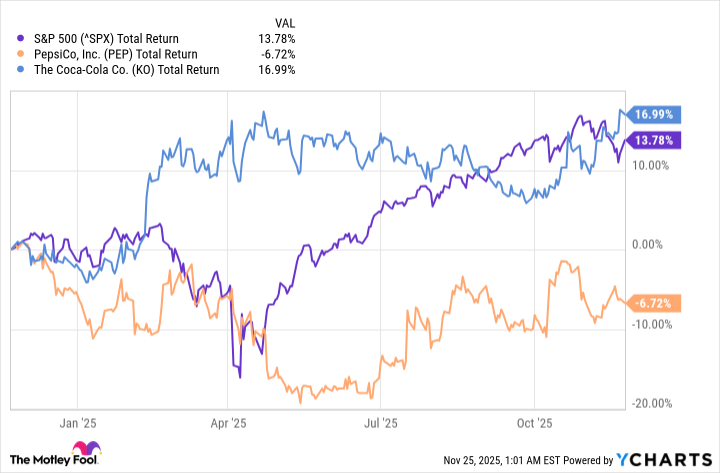

PepsiCo's momentum has slowed as FY2024 revenue rose only 0.4% to about $91.9 billion while GAAP net income increased ~6% to nearly $9.6 billion, leaving total returns trailing the S&P 500 and Coca-Cola over 1-, 3- and 5-year windows. Analysts forecast modest top-line growth of ~1.7% this year with GAAP EPS slipping from $8.16 to $8.11 next year; by comparison Coca‑Cola is modeled for ~2.9% revenue growth and EPS rising from $2.88 to $2.99. Despite a generous 3.9% dividend yield and Dividend King status, the firm’s slow fundamental growth and perceived “runner-up” positioning to Coca‑Cola are weighing on investor sentiment.

Market structure: PepsiCo’s mixed portfolio (snacks + beverages) creates bifurcated winners and losers — Coca‑Cola (KO) and lower‑cost private‑label beverage players gain pricing/positioning share in beverages while health‑forward brands and retailers with strong fresh/snack alternatives benefit in snacks. PepsiCo’s 0.4% revenue growth in 2024 and 3.9% dividend yield imply defensive bond‑like flows, reducing its equity beta versus growth names but weakening pricing power if promotional intensity rises. Commodity moves (corn, sugar, vegetable oil) and FX exposure in LATAM/APAC will transmit to margins; tighter crop supply or oil spikes compress snack margins faster than syrup‑focused peers. Risk assessment: Tail risks include sugar/fat taxes in key EM markets, packaging regulation raising capex, and a severe crop shock (e.g., +20% corn price) that could cut gross margin by 150–300bps. Short term (days–weeks) risk is sentiment/analyst revisions around earnings; medium term (3–12 months) depends on SKU innovation and SKU rationalization; long term (>12 months) hinges on portfolio shift into healthier SKUs or material M&A/divestiture. Hidden dependency: shelf‑space and retailer promo cadence — more trade spend to defend volume will hit FCF and buybacks. Trade implications: Tactical pair trade — long KO, short PEP — captures relative operational clarity: consider a dollar‑neutral 6–12 month position (equal $ exposure) with stop if spread moves >8% adverse. Options: sell KO 30–60 day cash‑secured puts ~5% OTM to harvest yield (target annualized carry >6%) and buy PEP 3‑month put spreads funded by selling nearer‑dated calls to limit cost. Rotate 1–3% portfolio weight from broad consumer staples into KO and into select health‑snack innovators (MDLZ, private) over 4–12 weeks. Contrarian angles: The market underweights PEP’s snack moat and recurring cash flow — if PEP executes modest pricing + mix shift that lifts organic revenue to >2% and EPS >$8.40 in next 12 months, re‑rating is likely and shorts would be punished. The current gap vs KO (PEG 5.4 vs 2.3) may be overdone if management levers promo and innovation to restore growth; conversely, if PEP misses by >2ppt on revenue growth or cuts dividend guidance, downside accelerates. Key trigger watches: 60‑day EPS revision delta >±3%, commodity cost moves >10%, and a formal strategic pivot or spin announcement.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment