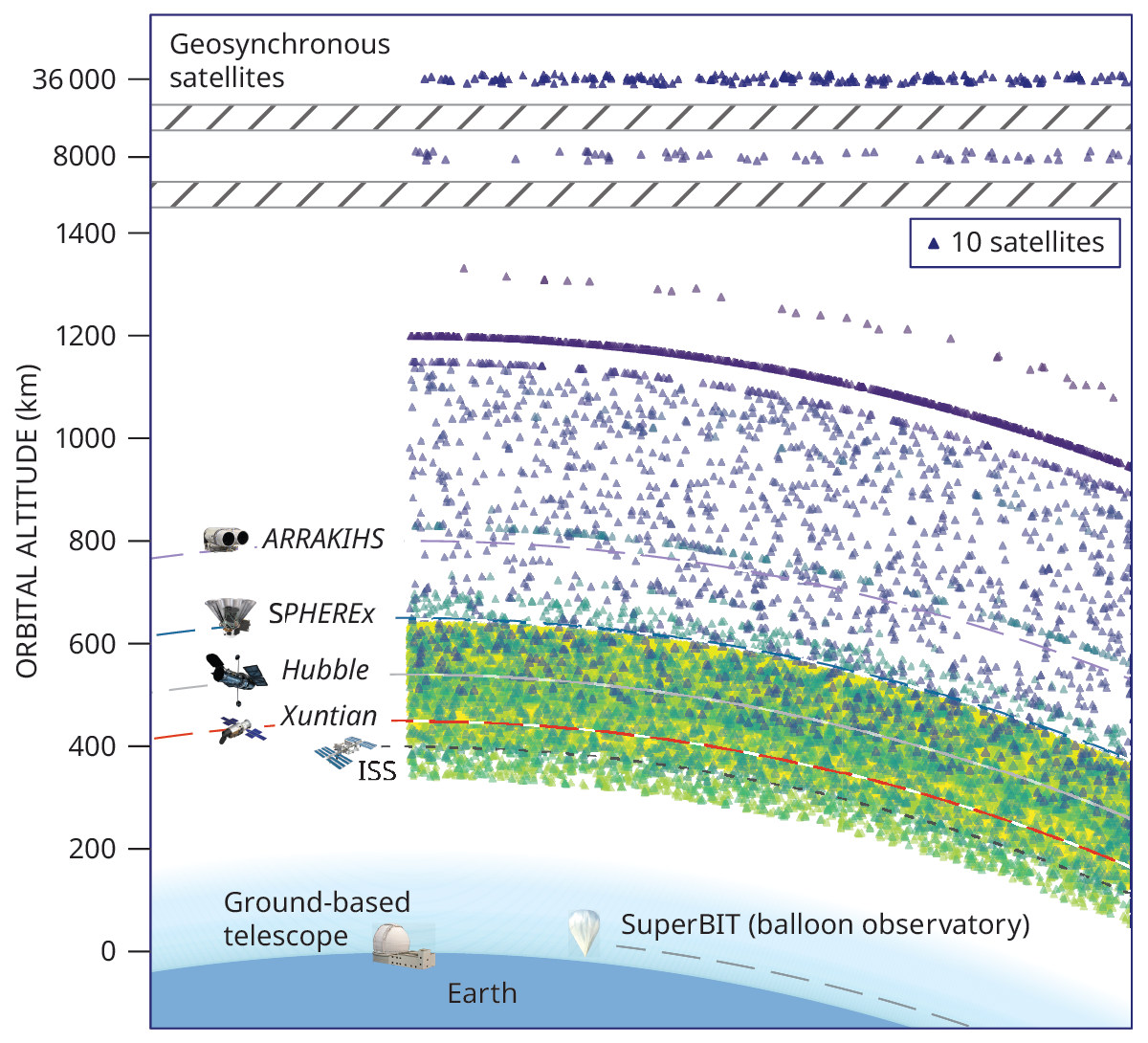

Rapid growth in commercial telecommunications constellations has lifted the number of active satellites from fewer than 2,700 in early 2020 to roughly 15,000 today, with filings that could push orbital populations to half a million+ by 2040. A simulation found that if proposed satellites are deployed as planned, 30% of Hubble exposures and 96% of images from three other space telescopes would contain at least one satellite trail, threatening data quality for astronomy. There is currently no single regulatory authority for orbital traffic, and mitigation recommendations include lower-altitude deployments and reduced satellite reflectivity—factors investors should monitor for potential regulatory, reputational, and operational impacts on satellite operators and related industries.

Market structure: Rapid LEO satellite buildouts favor launch and systems suppliers (satellite manufacturers, propulsion, ground-segment integrators) while compressing unit economics for connectivity providers. Expect downward pressure on per-subscriber ARPU for LEO internet over 1–5 years as supply (launch cadence, reusable rockets) outpaces clear demand; incumbents with scale (capable of absorbing capex) gain pricing power. Cross-asset signals: higher sector capex implies incremental corporate bond issuance and wider insurance/reinsurance spreads; implied volatility should rise for aerospace names on operational/regulatory news. Risk assessment: Tail risks include a Kessler-like collision cascade or a high-profile collision/insurance loss that triggers regulatory moratoria—both low probability but capable of wiping out specific equity cohorts in months and collapsing launch cadences for 6–12+ months. Near-term (30–180 days) catalysts: FCC/ITU guidance and IAU recommendations; medium-term (1–3 years) catalysts: major collisions or demonstrated low-reflectivity tech. Hidden dependencies: assumed satellite albedo, adherence to de-orbit rules, and concentrated launch capacity (SpaceX bottleneck) materially change outcomes. Trade implications: Direct trades should favor defense primes and imagery/systems providers that can monetize increased demand for space situational awareness (SSA). Short-duration option hedges on large-cap consumer tech with heavy Kuiper/space spend (AMZN) can protect portfolios versus capex surprise. Rotate from pure consumer tech cyclicality into defense (NOC, LMT, LHX) and specialist suppliers (MAXR, RKLB) over 6–24 months. Contrarian angles: The market underestimates consolidation and regulatory capture: stricter rules will favor large incumbents able to comply, creating durable oligopolies in compliant launches/SSA services. Analogous to telecom overbuild (post-2000 consolidation), expect M&A among smaller constellation operators and premium valuations for dark-satellite/anti-reflective technology licensors; this is a 2–5 year structural alpha opportunity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Ticker Sentiment