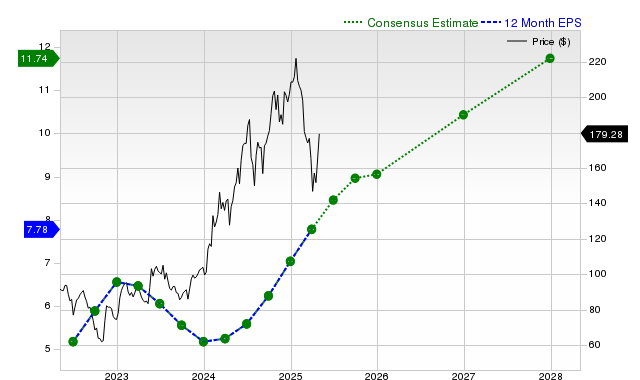

Taiwan Semiconductor Manufacturing (TSMC) has seen its stock rise 17.5% in the past month, outperforming the S&P 500 and its industry. Analysts' earnings estimates for the current quarter and fiscal year have increased by 2.6% and 2.1% respectively, projecting EPS growth of 54.7% and 30.5%. Despite strong revenue growth and a history of beating estimates, TSMC's Zacks Rank of #3 suggests it may perform in line with the broader market in the near term, and its valuation is at a premium compared to peers.

Taiwan Semiconductor Manufacturing Company Ltd. (TSM) has demonstrated significant recent stock appreciation, returning +17.5% over the past month, substantially outperforming both the Zacks S&P 500 composite's +5.2% gain and its own Zacks Semiconductor - Circuit Foundry industry's +16.3% rise. This investor interest is supported by positive revisions to earnings estimates; the Zacks Consensus Estimate for the current quarter's earnings per share (EPS) is $2.29, representing a +54.7% year-over-year increase, and has risen by +2.6% over the last 30 days. Similarly, the consensus EPS estimate for the current fiscal year stands at $9.19, a +30.5% projected increase from the prior year, with this estimate revised upwards by +2.1% in the past month. Projections for the next fiscal year also show a +14.8% EPS growth to $10.55, with a +2% upward revision in the last month. Revenue growth forecasts are robust, with consensus estimates pointing to a +42.5% year-over-year increase to $29.66 billion for the current quarter, and full-year revenue growth of +28.2% and +14.8% for the current and next fiscal years, respectively. TSMC has a strong track record, having beaten consensus EPS estimates in each of the trailing four quarters and topped consensus revenue estimates over the same period; the last reported quarter showed revenue of $25.53 billion (+35.3% YoY, +0.87% surprise) and EPS of $2.12 (+4.43% surprise). Despite these strong fundamental indicators and growth prospects, the company is rated Zacks Rank #3 (Hold), suggesting its near-term performance may align with the broader market, and its valuation is considered at a premium to peers, as indicated by a Zacks Value Style Score of D.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment