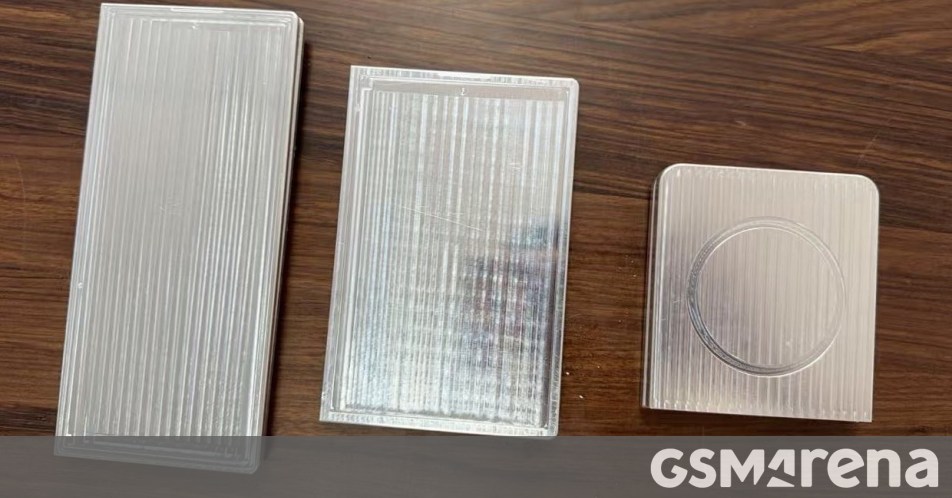

Samsung’s Galaxy Z Fold8 and Galaxy Z Flip8 are expected later this year, with a rumored third foldable, the Galaxy Z Fold8 Wide, also potentially launching. Leaked dummy units suggest only incremental design changes for the Fold8 and Flip8, while the Wide model could be shorter and slightly wider with a 4.7:3 outer-screen aspect ratio and 4:3 inner display. The article also hints at possible magnetic wireless charging support, but the information remains based on leaks rather than confirmed specifications.

The market takeaway is not the industrial design update itself; it is that Samsung is signaling a three-SKU foldable strategy, which matters for channel mix and ASP dispersion. A wider-format model tends to broaden the addressable use case from “status device” to “laptop-adjacent productivity device,” which can lift attach rates for stylus, keyboard, and case ecosystems while also increasing bill-of-materials complexity. That usually benefits component suppliers with pricing power in hinges, ultra-thin glass, batteries, and advanced camera modules more than the handset OEM, because the OEM is forced to absorb launch costs while trying to defend premium pricing.

The second-order risk is cannibalization inside the premium Android stack. A wider foldable at a likely higher price point can pull demand from the standard Fold variant and from large-screen slab flagships, but the more important effect is pressure on competitors that cannot match Samsung’s supply chain depth in foldables. If the form factor proves sticky, Chinese OEMs may accelerate copycat launches within 2-3 quarters, but they typically enter with weaker software optimization and lower gross margin, which caps their ability to scale profitably.

From a timing perspective, the near-term catalyst window is the launch cycle and first 6-8 weeks of channel checks; that is when sell-through, not just preorders, will reveal whether the wider aspect ratio is incremental or merely novelty. The bearish case is that the higher-thickness design and premium price ceiling limit mass-market adoption, especially if magnetic charging is more marketing than functionality and adds cost without materially improving battery anxiety. Over 12-18 months, the real valuation driver is not unit growth alone but whether Samsung can reset premium Android pricing higher without demand elasticity breaking.

The contrarian view is that the consensus may be underestimating ecosystem lock-in: a successful wider foldable can increase replacement stickiness and accessory monetization even if handset unit growth is modest. In that case, the winner is less the handset margin line and more the broader Android premium stack, where software, display, hinge, and power-delivery suppliers can capture recurring content per device.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05