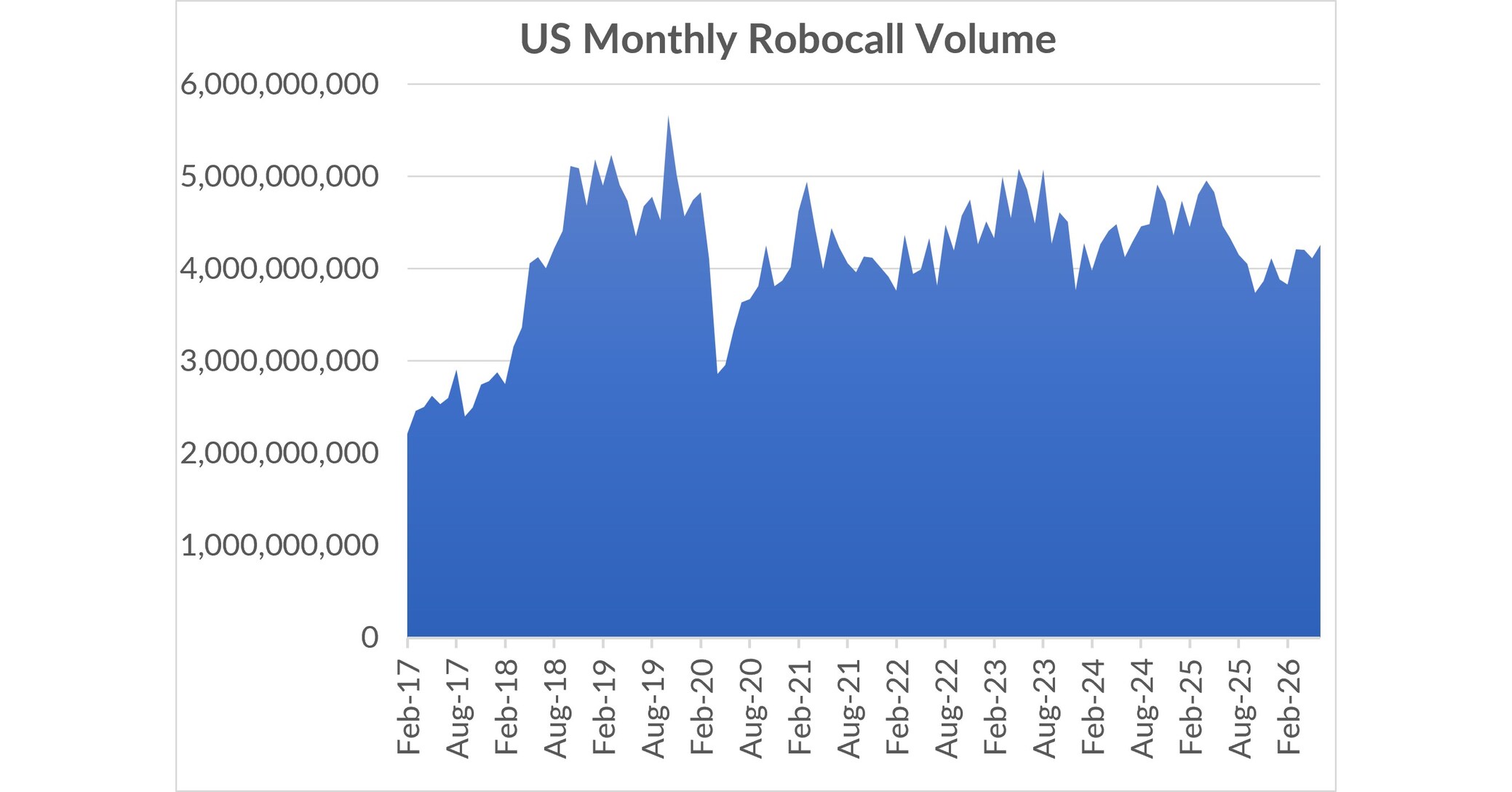

YouMail reports U.S. consumers received just over 4.25B robocalls in June 2026 (+3.4% vs May, -4.6% YoY), averaging 141.8M calls/day and 1,642 calls/sec. Over the 12 months, total robocalls fell to 48.7B, the lowest 12-month total since Nov 2022, though June remains the highest monthly volume since Jul 2025. Unwanted robocalls remain elevated at roughly 2B per month, with debt-consolidation loan scams (e.g., “Silver Oak Loans”) generating well over 30M calls in June.

The investable takeaway is not the raw call count; it is the behavioral tax on any model that still relies on cold outbound voice. As consumers harden their filters, answer rates fall and the economics deteriorate for debt settlement, subprime credit, insurance, home services, and collections-heavy businesses. That shifts budget toward authenticated channels and omnichannel platforms, which is directionally supportive for CPaaS/contact-center tooling such as TWLO and NICE, while pressuring voice-first lead-gen and telesales conversion rates. I would not overtrade a single-month bounce. The longer-run trend still signals a contained problem, so the near-term earnings impact for carriers or consumer names is likely de minimis. The more relevant catalyst path is 1-3 months: if the trend keeps drifting up, regulators may renew pressure on call-authentication and anti-spoofing, forcing incremental spend by carriers and enterprises; that is a slow-burn operating expense story, not a day-one revenue catalyst. Contrarian view: the market is likely to overfit this as a rising-fraud headline, when it is more plausibly noise around a still-low baseline. If the next two prints revert, any bid for anti-scam/security vendors should fade. Falsifiers are simple: a sustained 3-month acceleration, a new FCC enforcement action, or a material change in carrier screening standards.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

-0.10

Ticker Sentiment