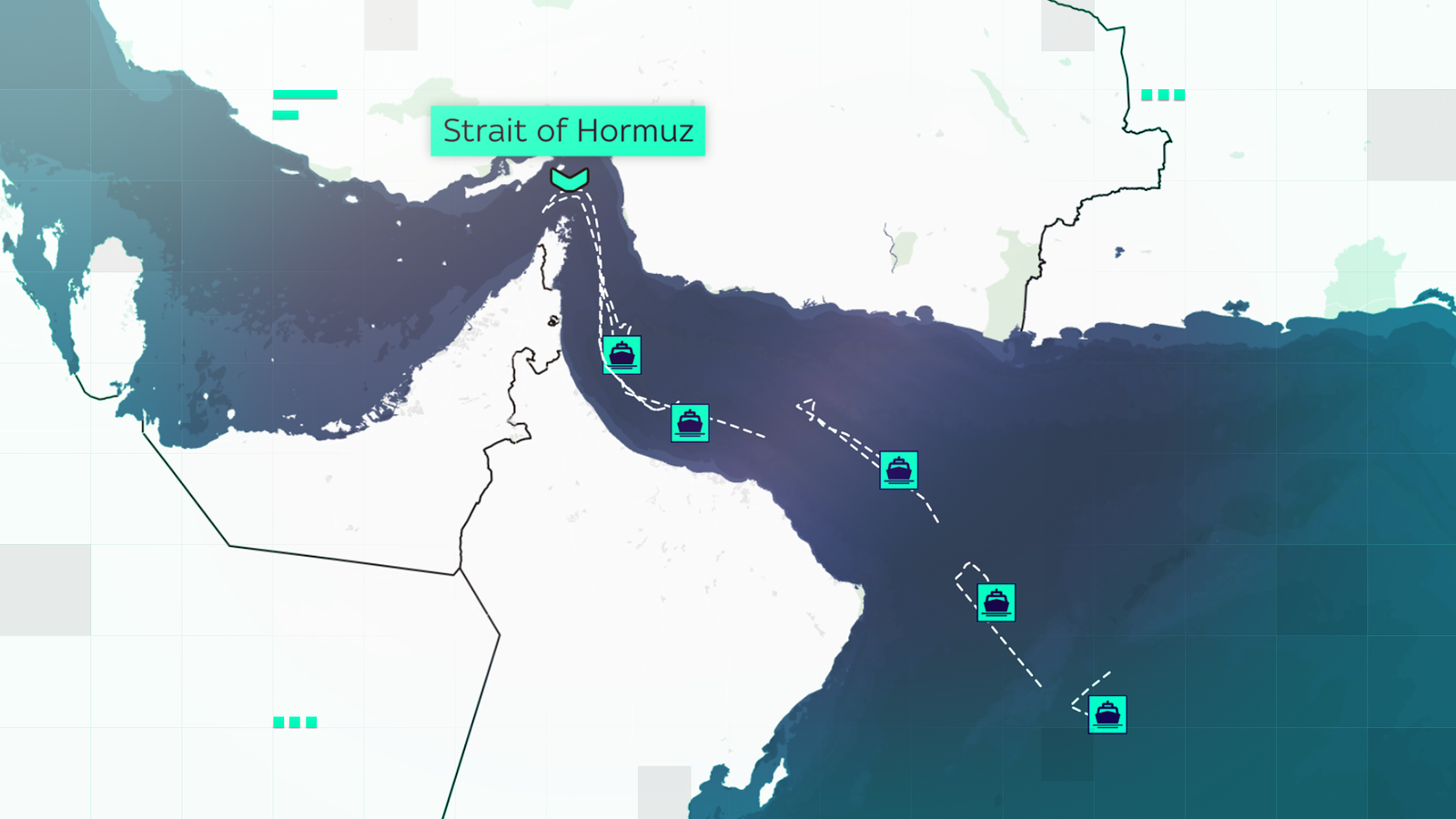

Maritime traffic through the Strait of Hormuz has been largely disrupted following US‑Iran strikes, with AIS interference and an attack on the Palau‑flagged tanker The Skylight forcing evacuations and US Navy warnings. The waterway normally transits about 20 million barrels a day (roughly one‑fifth of global oil) and analytics firm Kpler says five tankers turned back could carry around 10 million barrels, posing immediate upside risk to oil prices and material disruption to trade and logistics flows.

Market structure: a chokepoint shock — the Strait of Hormuz carries ~20m bbl/day so even limited disruptions (Kpler’s ~10m bbl on five tankers) creates immediate regional tightness and a temporary backwardation in Brent/WTI spreads. Short-term winners: large integrated producers and storage/transport owners (ability to re-route cargo, higher freight/insurance spreads). Direct losers: Asian refiners dependent on Gulf crude, airlines/cruise lines with fuel exposure, and export-dependent EM currencies; pricing power shifts to non-Gulf suppliers and to owners of spare tanker/storage capacity.

Risk assessment: tail scenarios include a >2‑week effective closure leading to a 10–30% surge in Brent (rough scenario +$10–$30/bbl) and knock-on inflation forcing central bank hawkishness. Immediate (days): volatility in crude and freight; short-term (weeks–months): inventory draws, shipping-rate spikes, insurance premium normalization; long-term (quarters–years): supply-chain re-routing, permanent higher freight/war-risk premiums and capex shifts into US exports/pipelines. Hidden risks: AIS spoofing hides true flows, derivatives positions in crude/options may be more concentrated than public data shows. Catalysts: further strikes, insurer war-risk declarations, or OPEC+ output responses.

Trade implications: tactical: buy short-dated Brent exposure (CME Brent futures or BNO) and 3‑month Brent 25‑delta call spreads; size 1–3% of fund NAV, enter within 48–72 hours, trim if Brent +25% or >$95. Equity plays: 3–5% long tanker owners (FRO, EURN, INSW) on 4–12 week horizon and 2–4% long energy majors (XOM, CVX) for 1–3 months; short 1–2% exposure to airlines (AAL, DAL) or buy 3‑month put spreads. Options: buy volatility — 3‑month Brent straddle or buy calls and sell nearer-term calls to monetize implied vol term-structure.

Contrarian view: market may overprice a permanent supply loss — past tanker/tension episodes (2019 tanker attacks) caused sharp but short-lived spikes; full rerouting via Cape of Good Hope raises freight costs and delivery times (~+7–10 days) but does not remove barrels long-term. Risks to the bullish oil trade: sustained Brent >$90 will accelerate US shale restart and demand destruction; avoid extended outright long on equities exposed to Asian refining until flow patterns and insurance premiums stabilize (2–6 weeks).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.65