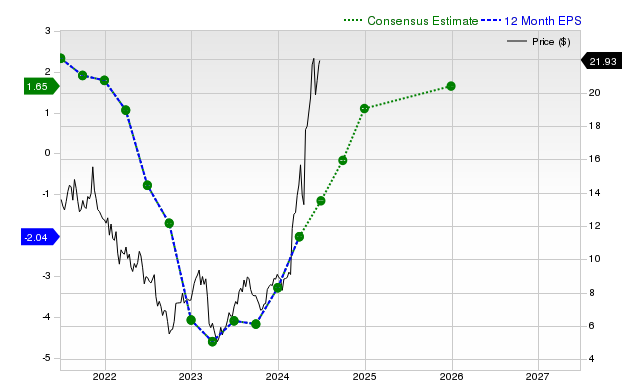

Tutor Perini (TPC) is attracting significant investor interest, with its shares up 20.6% over the past month, considerably outpacing the S&P 500 and its industry. The construction firm recently reported substantial beats on revenue and EPS for its last quarter, and consensus estimates project robust earnings growth of 155.9% for the current fiscal year and 76.6% for the next. This positive outlook, coupled with a Zacks Rank #1 (Strong Buy) rating and a B-grade valuation indicating trading at a discount to peers, suggests TPC is positioned for potential near-term outperformance.

Tutor Perini (TPC) is exhibiting strong bullish signals, underscored by significant stock outperformance and robust fundamental metrics. Over the past month, its shares have surged 20.6%, substantially outpacing both the S&P 500's 5.1% gain and its heavy construction industry peer group's 10.3% rise. This momentum is backed by a powerful recent earnings report, where TPC delivered revenues of $1.25 billion (+18.8% YoY) and an EPS of $0.53, representing a staggering 783.33% surprise over consensus. The forward outlook remains highly positive, with consensus estimates projecting monumental full-year EPS growth of +155.9% and a further +76.6% in the next fiscal year, supported by anticipated revenue growth of +18.6% and +17%, respectively. Despite this, it is noteworthy that these estimates have remained unchanged over the last 30 days. Valuation appears attractive, as the company's 'B' grade from Zacks for value suggests it trades at a discount to its peers. However, a potential point of caution is its inconsistent history of topping revenue estimates, having done so only once in the last four quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment