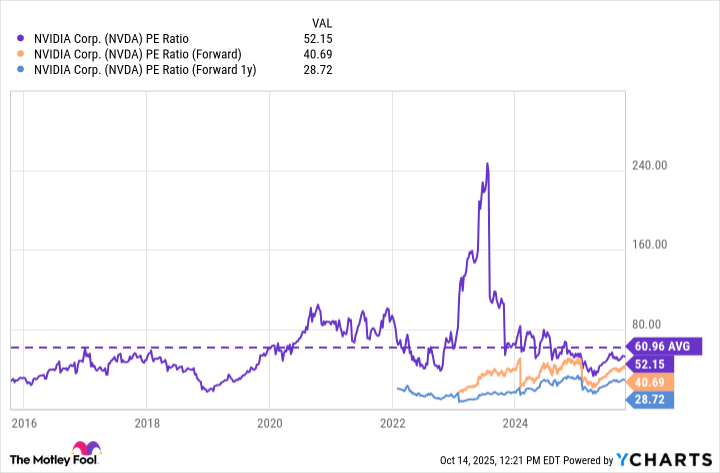

Nvidia is positioned for continued growth, with its upcoming fiscal Q3 2026 earnings report on November 19 anticipated to be a significant catalyst due to explosive demand for its AI data center chips. The company projects Q3 revenue of approximately $54 billion, a 54% year-over-year increase driven primarily by its data center segment, alongside an estimated $1.24 EPS. Investors will closely monitor forward guidance, with Q4 revenue projected at $61.1 billion, as Nvidia's new Blackwell Ultra and future Rubin GPU architectures are designed to capture a dominant share of an estimated $4 trillion in data center spending by 2030. Despite trading near record highs, Nvidia's current P/E of 51.9 is below its 10-year average, and strong forward earnings estimates suggest potential for further stock appreciation if financial results continue to meet or exceed expectations.

Nvidia's Q3 FY26 earnings report on November 19 is expected to show robust performance, with projected revenue of $54 billion, a 54% year-over-year increase. This growth is primarily driven by its data center segment, contributing nearly 90% of revenue, fueled by explosive demand for AI chips. Wall Street consensus estimates an EPS of $1.24, reflecting 53% year-over-year growth. The demand surge stems from next-generation AI reasoning models requiring significantly more computing capacity. Nvidia's Blackwell Ultra GB300 GPUs offer 50x performance over older H100 chips, with the future Rubin architecture rumored to be 3.3x more powerful. CEO Jensen Huang forecasts a $4 trillion data center upgrade market by 2030, positioning Nvidia for a dominant share. Despite trading near record highs, Nvidia's current P/E of 51.9 is a 15% discount to its 10-year average of 60.9. Wall Street projects FY26 EPS of $4.50 and FY27 EPS of $6.38, yielding forward P/E ratios of 40.5 and 28.6. This implies substantial potential for stock appreciation, with an estimated 113% upside to align with its historical P/E based on future earnings. Investors should closely monitor Nvidia's Q4 FY26 forward guidance, with Wall Street anticipating $61.1 billion in revenue. Exceeding this forecast, coupled with strong Q3 results, would act as a significant bullish catalyst. Continued strong financial performance is crucial for the market to price in Nvidia's future potential.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

extremely positive

Sentiment Score

0.90

Ticker Sentiment