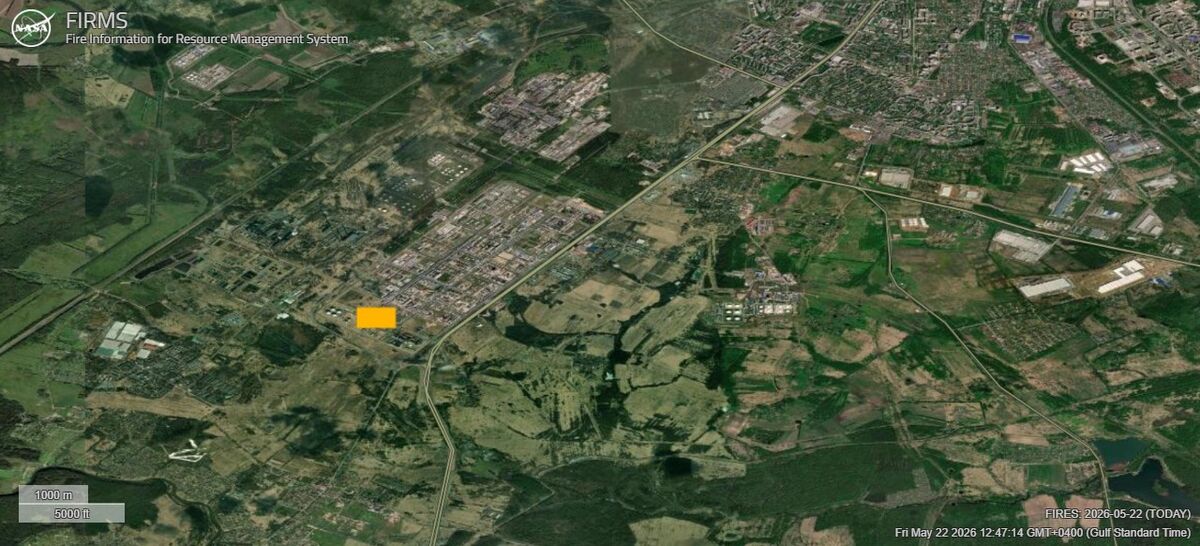

Ukraine said it used long-range drones to strike Russia’s Yaroslavl oil refinery again overnight, targeting oil-processing and export infrastructure in central Russia. The attack adds to damage on Russia’s energy assets and underscores continued wartime pressure on fuel supply chains. The event is geopolitically significant and may keep a risk premium embedded in regional energy markets.

This is less a one-off headline than evidence of a persistent degradation campaign against the Russian downstream network. The second-order effect is that even when physical output losses are repaired, insurers, logistics operators, and export schedulers begin to price in a higher disruption premium, which can widen regional product spreads before outright crude supply is visibly impaired. The market usually underestimates how quickly repeated precision strikes can turn a refinery from a margin engine into a maintenance liability, especially when spare parts, catalysts, and specialized labor are constrained by sanctions. For energy markets, the more important transmission is refined-product tightness rather than crude scarcity. If Russian domestic processing is intermittently offline, Moscow can be forced to redirect more crude to export channels while exporting fewer middle distillates, which tends to support diesel cracks and raise volatility in European product benchmarks over the next 2-8 weeks. That dynamic is bullish for non-Russian refiners with access to discounted feedstock and complex conversion capacity, while transport-heavy sectors and European industrials face a small but real input-cost shock. The catalyst risk is escalation and cadence: a single strike matters little, but a sustained campaign against refineries and export nodes can create compounding downtime over 1-3 months. The main reversal is either improved point defense or a shift in negotiating dynamics that reduces strike intensity; absent that, the trade is not the spot price of Brent so much as the tail risk of refined-product shortages and higher crack spreads. The contrarian read is that the market may be overfocused on headline crude disruption and underpricing the duration of maintenance friction, which is exactly where margins get repriced. From a risk-management lens, this is a volatility bid more than a directional crude shock, so the cleaner expression is through product exposure and relative value. The best payoff is to own complex refiners versus broad energy, while fading European industrials that are most sensitive to diesel and power-cost pass-through. If the campaign broadens or repeats over the next several weeks, the trade can work even without a large move in Brent because crack spreads and implied volatility should re-rate first.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35