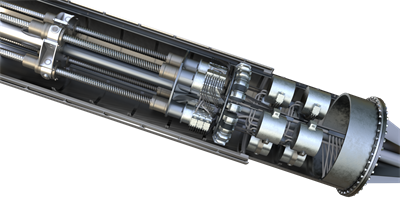

Ocean Harvesting Technologies AB is conducting a €1.0m share issue for 2026–2027 to fund development and prototype testing of its patent-protected InfinityWEC wave energy converter, primarily for personnel, external engineering, prototype equipment and IP management. The work is tied to two EU-funded CETP projects — INFINITY (€2.7m, 2025–2027) focusing on full-scale system and power-take-off validation in a 1:4 test rig, and WECHULL+ (€3.0m, 2024–2027) advancing a low-cost honeycomb concrete buoy for sea trials — positioning the technology toward sea trials and commercial deployment in utility-scale wave farms, island grids, industrial electrification and green hydrogen/ammonia production.

Market structure: Winners are specialist marine-energy developers (Ocean Harvesting), coastal utilities and offshore construction firms that can supply installation and grid-connection (expect +€0.5–2bn incremental tender pools in EU coastal markets annually if wave scales). Losers are marginal peaking-storage providers and projects whose economics rely on high curtailment arbitrage; widespread deployment of low-variability wave power could shave 5–15% off demand for short-duration battery cycling in local grids. Competitive dynamics favor low-cost, locally manufactured buoys (honeycomb concrete + EPS) which, if validated, compresses LCOE toward onshore wind levels and raises barriers to exotic WEC designs that require expensive materials. Risk assessment: Tail risks include prototype failure, major sea-trial damage (>€10–30m loss), IP litigation, or a withdrawal of EU CETP funds (risk window next 6–18 months). Immediate impact is negligible to public markets; short-term (6–24 months) outcome hinges on 1:4 scale rig validation and sea trials; long-term (2–5 years) commercialization depends on supply-chain scale and grid permitting. Hidden dependencies: reliance on partner engineering capacity, local concrete/EPS supply, and permitting timelines (can add 12–36 months). Key catalysts: successful 1:4 rig results (target within 12 months), WECHULL+ sea trials (within 12–24 months), and additional EU/industry offtake or EPC partner commitments (>€5m+). Trade implications: Direct speculative plays: small-cap marine-energy equities (e.g., OPTT) and offshore-integrator names (Ørsted ORSTED.CO, Vestas VWS.CO, Siemens Energy SIE.DE) should be overweight relative to pure storage miners (e.g., LIT ETF). Use milestone-based sizing: starter 25–50% now, add on validated sea-trial news. Options: use 12–24 month call spreads on small-cap marine names to cap downside; buy protective puts on storage/miner exposure if implementing a pair trade (long ORSTED, short LIT). Rotate 1–3% portfolio weight from battery/EV supply chains into offshore infrastructure over 6–18 months. Contrarian angles: Consensus underestimates deployment friction—local manufacturing and permitting can blow out unit cost by 20–40%, replicating tidal energy’s long path to scale (MeyGen took >7 years). Public markets likely underprice binary operational risk but also underappreciate upside if EU scales factory-based buoy production (could drive private valuations +3–5x if CAPEX/OPEX targets proven). Unintended consequence: rapid coastal rollouts could trigger environmental/regulatory pushback raising timelines and financing costs; prefer milestone-based entry and caps on exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35