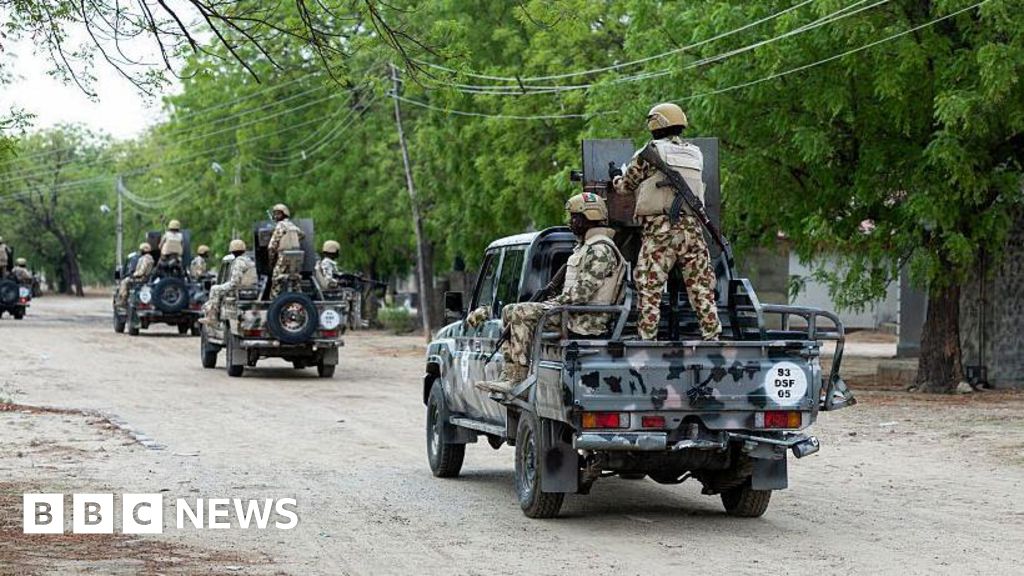

Nigeria and US forces killed senior Islamic State leader Abu-Bilal al-Minuki in a joint operation in the Lake Chad Basin, a setback for IS command structure and African networks. Nigerian officials said the strike was enabled by recent US-Nigeria intelligence sharing and partnership, and that al-Minuki was linked to IS operations across the Sahel and West Africa. The event is security-positive for Nigeria and the region, but the market impact is likely limited outside defense and geopolitics.

This matters less as a discrete counterterrorism event than as a signal that the US is willing to use Nigeria as an operational hub for pressure on trans-Sahel jihadist logistics. That raises the near-term cost of coordination for IS-affiliated cells: leadership attrition is most damaging when paired with intelligence fusion, because it interrupts courier networks, cross-border movement, and finance routing for 1-3 quarters even if the group can replace personnel. The second-order effect is asymmetric for the region’s security beneficiaries. Nigeria’s military and intelligence services gain credibility and likely unlock incremental external support, but the bigger marginal winner is any government or contractor tied to border surveillance, ISR, drones, secure comms, and convoy protection across the Lake Chad basin. Conversely, local transport, agriculture, and telecom operators in the northeast remain exposed to retaliation risk because militant groups tend to shift from high-profile leadership targets to softer civilian and infrastructure targets after a decapitation event. The market is likely underpricing the policy signal to US Africa security posture. If Washington and Abuja are formalizing joint targeting, that increases the probability of more frequent strikes, training packages, and procurement tied to mobility, surveillance, and air support over the next 6-12 months. The contrarian risk is that this is tactically effective but strategically marginal: militant groups in the Sahel are fragmented, and pressure in one theatre can displace violence into Niger, Chad, or Cameroon, so headline wins may coexist with worsening regional volatility. From a positioning standpoint, this is not a broad EM long; it is a selective defense-and-security-services story with optionality on recurring cooperation. The cleanest expression is to buy on any pullback names leveraged to border security and ISR rather than general contractors, while fading local consumer and transport exposures if you expect retaliatory attacks to follow within weeks. The best risk/reward is in options, because the catalyst path is lumpy: either cooperation deepens and budgets re-rate, or the event fades and premium decays quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.20