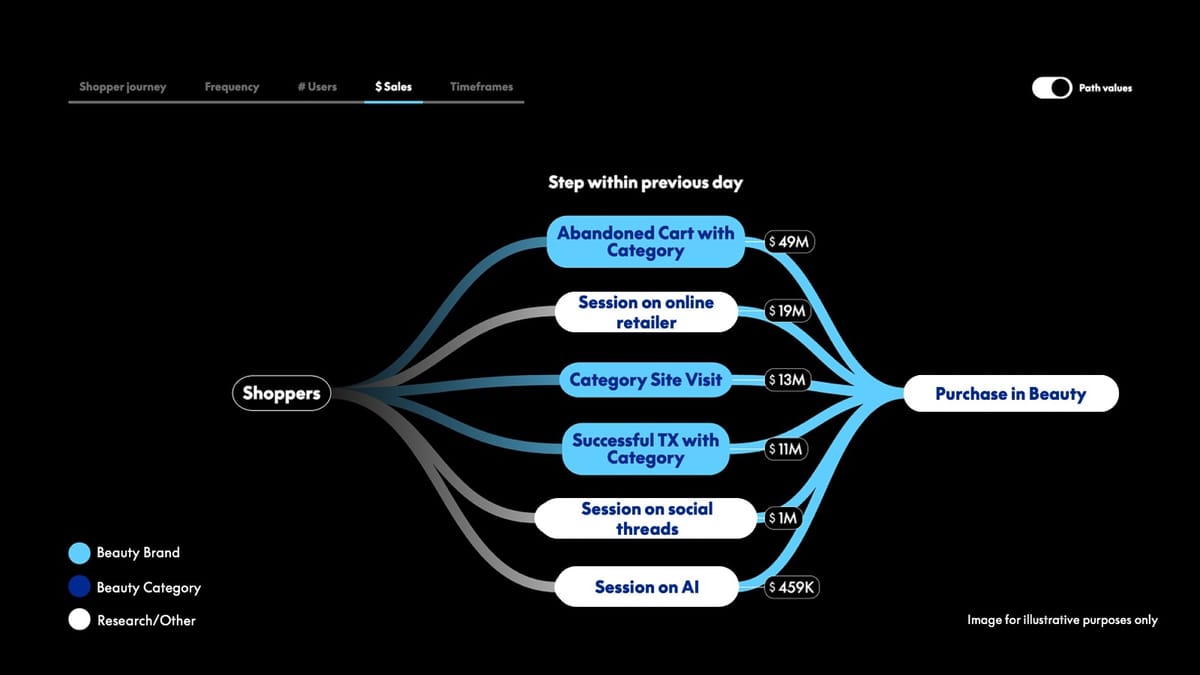

PayPal launched Transaction Graph Insights & Measurement on January 6, 2026, offering advertisers deterministic, cross-merchant visibility built on a transaction graph that connects more than 430 million consumer accounts and tens of millions of merchants. The suite includes interactive analytics, a first-party measurement product using deterministic identity, and a partner validation program (AppsFlyer, Cint, Experian, iSpot, Kantar, Kochava, LiveRamp); early results include Ulta Beauty reporting a 20% uplift in transaction spend and an independent Lucid validation showing a 136% lift in brand favorability. The product targets measurement gaps in platform-specific attribution, launches immediately in the U.S. with planned expansion to the U.K. and Germany, and may reshape ad attribution and commerce-media competition while raising data-privacy and regulatory considerations.

Market structure: PayPal (PYPL) gains structurally as a cross‑merchant signal provider with deterministic identity across 430M accounts, likely enabling a 5–15% reallocation of advertiser budgets from platform-specific retail/social media to commerce media over 12–24 months. Winners include PYPL, LiveRamp (RAMP), measurement partners (CINT) and programmatic suppliers (PUBM, TTD) that enable offsite ad scale; pure retail‑media islands (merchant‑only networks) and probabilistic adtech vendors face pricing pressure on low‑accuracy inventory. CPMs for verified purchase‑driven inventory should rise 10–25% as demand outstrips immediate deterministic supply. Risk assessment: Tail risks are regulatory curbs on financial‑data advertising (GDPR/FTC actions) or a major data breach; a conservative scenario (10–30% ad revenue haircut) could wipe 5–10% off PYPL EPS in a year. Short window impact: positive sentiment and bid‑driven equity lift in days; medium term (3–9 months) hinges on merchant onboarding and partner certifications; long term (12–36 months) depends on network effects and consent regimes. Hidden dependency: success requires merchant opt‑ins and consumer consent—without ~20–30% merchant participation in key categories, deterministic scale limits accuracy. trade implications: Direct play: overweight PYPL equity and select call spreads (6–9 month) to capture ad revenue diversification; tactical longs in RAMP/CINT and programmatic suppliers (PUBM/TTD) for measurement/inventory demand. Pair trade: long PYPL or MA (1–3% risk) vs short META (1–2%) over 12 months expecting partial budget migration; use defined‑loss option structures if regulatory binary risk is high. contrarian angles: The market may overestimate immediate scale — deterministic identity sacrifices reach, so short‑term PYPL multiple expansion could be overdone if merchant uptake <20% in 6 months. Conversely Mastercard (MA) is an underappreciated competitor with broader bank partnerships and could capture enterprise commerce media share; regulatory backlash is a real catalyst that could re‑route value to banks/card networks rather than PayPal.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment