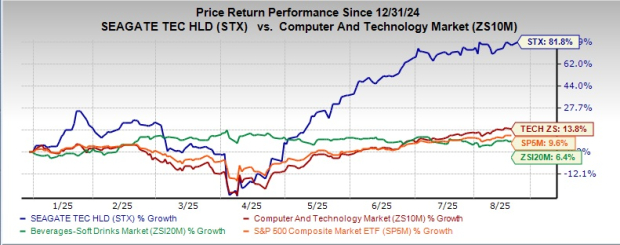

Seagate Technology (STX) shares have surged 81.8% year-to-date, significantly outperforming peers, fueled by a 40% year-over-year increase in mass capacity revenues to $2 billion, primarily from nearline cloud demand. The company is leveraging AI-driven data center expansion and advancing its HAMR technology, targeting 44TB platforms by 2026, which contributed to a record 37.9% gross margin. Despite strong operational performance and plans for share repurchases, STX faces headwinds from $5 billion in long-term debt, intense competition, and macroeconomic uncertainties, warranting a cautious outlook.

Seagate Technology (STX) has demonstrated significant market outperformance, with its stock gaining 81.8% year-to-date, substantially exceeding its peers and sector benchmarks. This surge is fundamentally supported by strong operational results, particularly in its mass capacity storage segment, where revenues increased 40% year-over-year to $2 billion, driven by accelerating demand from cloud service providers for AI-ready infrastructure. The company's nearline products constituted 91% of mass capacity exabytes shipped, underscoring its pivotal role in the AI data ecosystem. This operational strength translated into a record gross margin of 37.9%, an improvement of 700 basis points year-over-year, bolstered by pricing initiatives and a favorable product mix. Management's confidence is further signaled by a robust Q1 revenue forecast of approximately $2.5 billion, representing 15% year-over-year growth, and the planned resumption of share repurchases. However, significant headwinds temper this positive outlook. The company carries a substantial long-term debt of $5 billion against a cash position of $891 million, which could constrain strategic flexibility. Furthermore, STX faces intense competition, foreign currency exposure, and broader macroeconomic uncertainties. While fiscal 2026 and 2027 earnings estimates have seen upward revisions, the stock's forward P/E of 14.77x, though below the industry average, is notably above its own historical mean, reflecting a market that has already priced in significant growth expectations.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.20

Ticker Sentiment