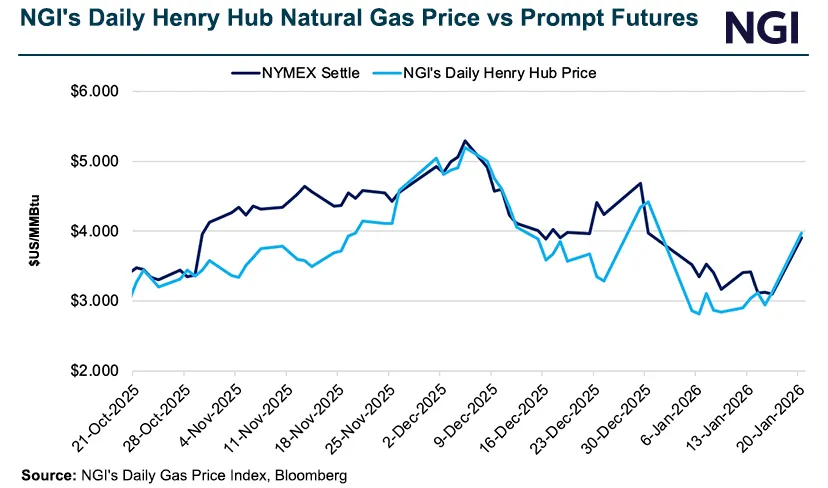

Prompt-month February Nymex natural gas futures climbed sharply, trading up $0.857 to $4.764/MMBtu as of 12:08 p.m. ET after a 26% surge the prior day. The secondary rally was driven by bitterly cold weather forecasts and worsening production freeze-offs that triggered another wave of short covering, signaling tighter near-term supply and elevated price volatility for natural gas markets.

Market structure: Front‑month NYMEX gas ripping to $4.76 signals immediate winners are US gas producers (EQT, CNX, SWN) and LNG exporters (LNG) who see prompt margin lift; midstream fee‑based names (WMB, KMI) gain from higher throughput and potential bottleneck rents. Losers include gas‑intensive power generators and industrials facing margin compression; elevated prompt pricing increases regional basis volatility and could lift power and heating fuel prices across commodities. Risk assessment: Primary tail risks are a warm snap collapsing front‑month gas toward <$3.50 within 7–21 days, or quick resolution of freeze‑offs that allows production to snap back, and conversely infrastructure failures or LNG demand surprise pushing prices >$6.50. Time horizons: immediate (days) dominated by short covering and weather models; short term (weeks) depends on EIA weekly withdrawals and NOAA forecasts; long term (quarters) hinges on storage refill pace and LNG export ramp. Trade implications: Tactical plays favor front‑month long exposure while volatility is rising — use defined‑risk call spreads on NYMEX NG (buy $5.00 / sell $7.50 4–8 week spread) or buy UNG as a proxy; add 1–3% directional equity exposure to CNX/SWN (3–6 month horizon) and 1–2% to WMB/KMI for midstream. Use pair trade long CNX, short NRG (1:1 notional) to isolate commodity upside vs generator demand risk; scale out if NG > $6.50 or if withdrawals fall <5 Bcf week‑over‑week. Contrarian angles: The market may be overpaying for a transient freeze‑off — historical episodic spikes (2018, 2021) reversed within 2–6 weeks when production returned and storage showed resilience. Watch for EIA inventory misses, LNG cargo cancellations, and pipeline maintenance notices — a lack of follow‑through would create a fade opportunity to short front‑month NG or trim E&P exposure into pop.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.60