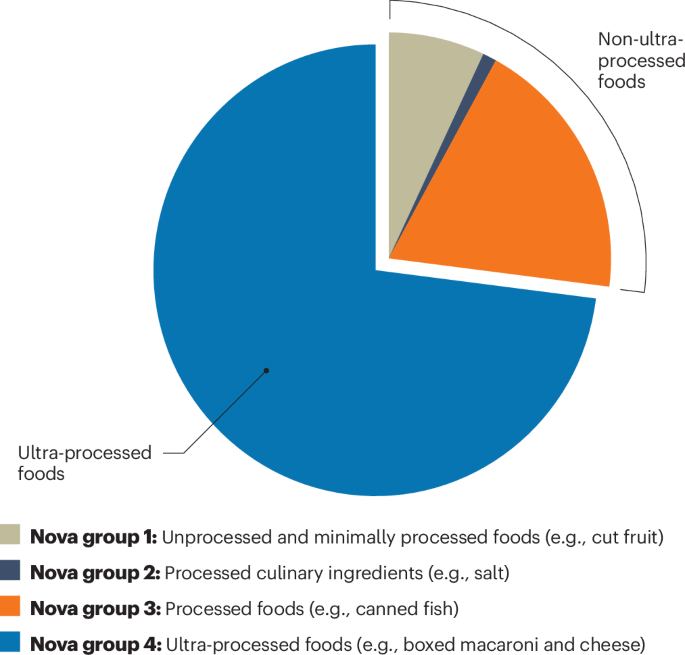

A Nature Medicine commentary by Moran, Khandpur and Roberto argues that policy should target definitions of 'non‑ultra‑processed' foods rather than attempting to classify 'ultra‑processed' items, asserting the former approach would better protect public health. The piece references WHO calls for guidelines and recent HHS/FDA/USDA attention to health risks from ultra‑processed foods, signaling heightened regulatory and public‑health scrutiny that could eventually influence labeling, guidance, or regulation affecting food manufacturers and retailers.

Market structure: A regulatory tilt from identifying “ultra-processed” to defining and promoting “non‑ultra‑processed” foods reallocates end‑market demand toward fresh, minimally processed and plant‑forward suppliers and retailers that can credibly claim healthier portfolios. Large branded packaged‑food incumbents (KHC, GIS, K, MDLZ, PEP snacks) face higher compliance and reformulation costs and potential excise/tax risk; margins could compress by 100–300bps over 12–24 months if labeling/tax measures are enacted at scale. Risk assessment: Tail risks include rapid policy action (WHO/FDA guideline + US municipal taxes) that could drop affected equities 15–30% within 3–12 months, or conversely slow consumer behaviour change leaving valuations intact. Short term (days–weeks) volatility will hinge on guidance publications (likely 30–90 day catalysts); long term (2+ years) corporate capex for reformulation and supply‑chain retooling will determine survivor economics. Hidden dependencies: private‑label and fast‑casual chains can quickly capture share, pressuring branded pricing power. Trade implications: Favor long exposure to retailers/wholesalers with fresh/organic scale (COST, KR) and to plant‑protein/health‑brand innovators (BYND, PBJ ETF) while hedging packaged food exposure via puts or credit protection on KHC/GIS; expect relative share shifts of 3–8% in category penetration over 12 months. Cross‑asset: increased demand for soy/protein and lower sugar/corn sweetener demand will modestly pressure commodity spreads; packaged‑food credit spreads could widen 20–50bps if regulation accelerates. Contrarian angles: Consensus assumes fast regulatory throughput; history (soda taxes, labeling rules) shows staggered, localized implementation—opportunity to sell short‑term fear and buy high‑quality staples on 10–20% dips. Also, brand loyalty and price sensitivity mean low‑income consumers may resist switching, protecting volume for low‑cost packaged players; this caps downside for blue‑chip staples and argues for selective hedges, not blanket shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00