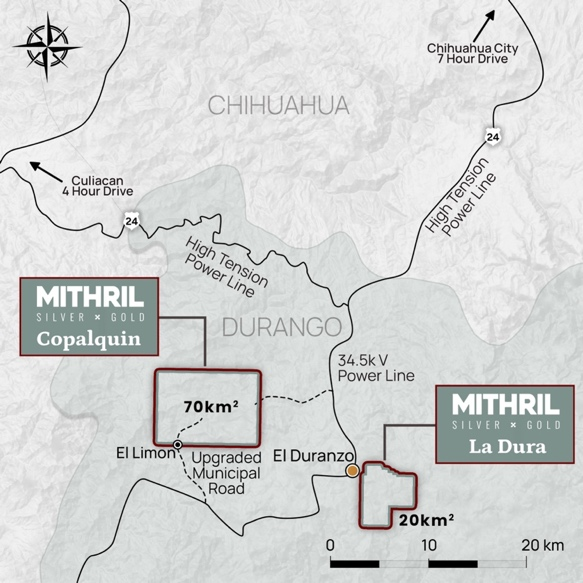

Mithril Silver and Gold reported successful exploration results at its Copalquin district in Durango, Mexico, confirming high-grade silver‑gold mineralisation at Target 5 (notable intercepts including 1.00 m @ 1,714 g/t AgEq (5.80 g/t Au, 1,308 g/t Ag) and 2.75 m @ 660 g/t AgEq) and extending the Target 1 resource ~300 m to the west while remaining open. The company has completed an aerial magnetic survey, commenced Phase IV drilling at Target 1 (~3,000 m) and started maiden drilling at Target 3, and plans up to 25,000 m of drilling in the first 6–8 months of 2026 to expand resources. Previously reported maiden resource at Target 1 totals Indicated 691 kt @ 5.43 g/t Au and 114 g/t Ag (121 koz Au, 2.538 Moz Ag) plus Inferred 1,725 kt @ 4.55 g/t Au and 152 g/t Ag (252 koz Au, 8.414 Moz Ag); Mithril holds an option to acquire 100% of the concessions for US$10M by 7 Aug 2028. These developments materially de‑risk the district-scale thesis and could drive near‑term market re‑rating for the company if subsequent drilling converts high‑grade intercepts into expanded resources.

MARKET STRUCTURE: Mithril (ASX:MTH / TSXV:MSG / OTCQB:MTIRF) is a potential winner—high-grade intercepts and a 25,000m campaign materially increase the probability of a multi-million-ounce district resource, improving M&A and re-rating prospects versus peers. Downstream winners include local service contractors in Durango and specialist high-grade silver juniors; losers are late-stage brownfield acquirers who pay premiums if Mithril proves scale. Commodity prices (silver/gold) likely unaffected near-term; company news will drive idiosyncratic volatility. RISK ASSESSMENT: Key tail risks are funding/dilution (company needs capital to exercise US$10M option by Aug‑7‑2028), metallurgical shortfalls, and Mexican tenure/security/regulatory issues; these carry >20% downside in adverse outcomes. Immediate (days) = news-driven spread/volatility; short-term (weeks/months) = assay cadence, aeromag report and Phase‑IV results; long-term (years) = resource-to-development and financing cycles. Hidden dependency: junior valuation is levered to gold:silver ratio and global junior financing windows. TRADE IMPLICATIONS: Direct play = small equity allocation to MTH to capture re‑rating on continued high‑grade results, plus volatility-defined option leverage if liquid. Pair trade = isolate company risk by going long MTH and short broad silver miners ETF (SIL) to hedge metal-price moves. Time entries ahead of aeromag/drill result clusters (next 2–12 weeks), trim 50% at +50% gains, stop-loss 30–35% on equity. CONTRARIAN ANGLES: Market may underprice dilution and execution risk—high‑grade hits often prompt funding raises that compress existing holders; hence options or capped-risk constructs preferred over large cash buys. Conversely, if aeromag confirms conduit structures and Phase‑IV validates continuity, re-rating could be >2x in 6–12 months—a classic high‑upside junior exploration asymmetric bet. Watch for equity raises >A$5M (sell signal) and metallurgical recoveries <85% (reassess).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55