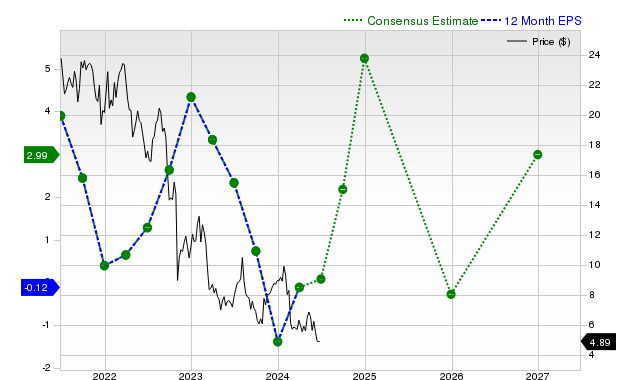

Gray Media (GTN) currently holds a Zacks Rank #4 (Sell), signaling potential near-term underperformance, despite its 'A' valuation score suggesting it trades at a discount to peers. The broadcast television company's shares declined 3.3% over the past month, underperforming the S&P 500, with current fiscal year EPS projected to fall 141.7% to -$1.4, though next fiscal year estimates anticipate a robust rebound with a 275.7% increase to $2.46.

Gray Media (GTN) presents a dichotomous investment profile, characterized by severe near-term fundamental weakness juxtaposed with a highly attractive valuation and a strong projected earnings rebound. The stock has underperformed, returning -3.3% over the past month against the S&P 500's +3.1% gain. This reflects a challenging current operating environment, with consensus estimates pointing to a significant current-quarter revenue decline of -21.4% and an earnings per share (EPS) loss of $0.41, a -147.7% year-over-year reversal. For the full current fiscal year, forecasts indicate a revenue drop of -14.6% and an EPS of -$1.40, down -141.7% from the prior year. This negative trend is reinforced by a poor recent history, including a significant -82.61% EPS miss last quarter and a Zacks Rank #4 (Sell), signaling likely near-term market underperformance. Conversely, the outlook for the next fiscal year is starkly different, with analysts forecasting a +275.7% surge in EPS to $2.46 alongside a +12.7% revenue increase. Furthermore, the company's 'A' grade on the Zacks Value Style Score suggests it is trading at a discount to its peers, creating a classic value-trap versus deep-value dilemma for investors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50

Ticker Sentiment