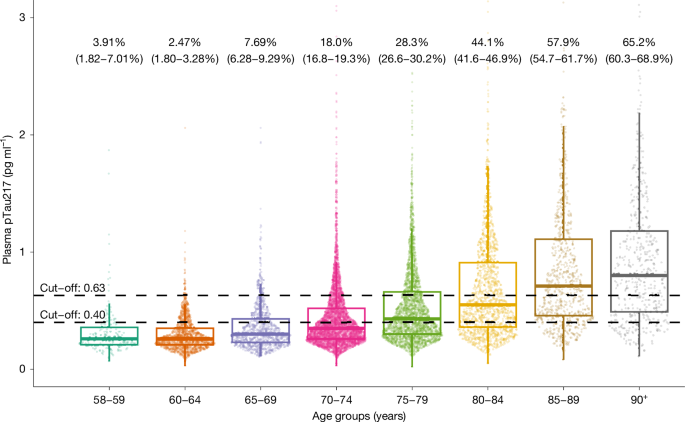

In a large Norwegian population study (11,486 plasma samples), plasma pTau217 was used to estimate Alzheimer’s disease neuropathological change (ADNC) prevalence: under 8% for ages 58–69.9, rising to 65.2% for those over 90, and 33.4% across the 70+ cohort. Within the 70+ group, 10.0% were classified as preclinical AD, 10.4% prodromal AD and 9.8% AD dementia; 909 of 8,949 (10.2%) met current eligibility criteria for disease‑modifying therapies (weighted estimate 11.1%). Findings highlight a sizeable addressable population for anti‑amyloid treatments, APOE ε4 and low eGFR associations with pTau217, and use of validated pTau217 cutoffs (0.40 and ≥0.63 pg/ml) — data that could inform demand forecasts, payer exposure and clinical adoption risk assessments for Alzheimer’s therapeutics.

Market structure: Winners are diagnostic and lab-platform vendors that scale blood pTau217 (QTRX, large clinical labs like LH) and tau-targeted biotech (ALEC, PRTA) that benefit from faster, cheaper case-finding; established PET-only gatekeepers and niche imaging vendors lose discretionary volume. Estimated addressable pool ~11% of 70+ (HUNT) implies demand shock for diagnostics and DMT monitoring—if extrapolated to US/EU seniors, incremental annual treated patients could be millions, pressuring infusion capacity and MRI/MCA monitoring budgets within 12–36 months. Risk assessment: Tail risks include major payer pushback (Medicare/CMS price/coverage limits) and assay-class action if PPV/NPV vary in diverse populations; both are low-probability but can cut peak revenue by 50%+. Short-term (0–3 months) volatility from guideline updates, medium (3–12 months) adoption/coverage decisions, long-term (1–5 years) structural demand for DMTs and diagnostics. Hidden dependency: renal dysfunction (eGFR <51) biases pTau217—market estimates that ignore CKD prevalence will misprice diagnostics adoption and payer risk. trade implications: Direct play: overweight QTRX (diagnostics platform) and select tau-biotech ALEC on 12–24 month horizon; underweight or hedge large AD therapeutics exposed names (BIIB) because pricing and uptake remain uncertain. Use pair trade long QTRX / short BIIB to capture diagnostic upside vs therapeutic pricing/regulatory risk. Options: 3–9 month call spreads on QTRX to limit capital and 3-month put spreads on BIIB as asymmetric downside protection. contrarian: Consensus overestimates immediate treated population—real-world uptake likely 20–40% of eligibility in first 2 years due to access, adverse events (ARIA) and payer constraints; diagnostics upside is underpriced today. Historical parallel: PET adoption took >5 years—blood-based tests may compress to 1–3 years but only with favorable reimbursement; unintended consequence: rapid case-finding could trigger tougher price negotiations that cap long-term drug upside.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment